Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

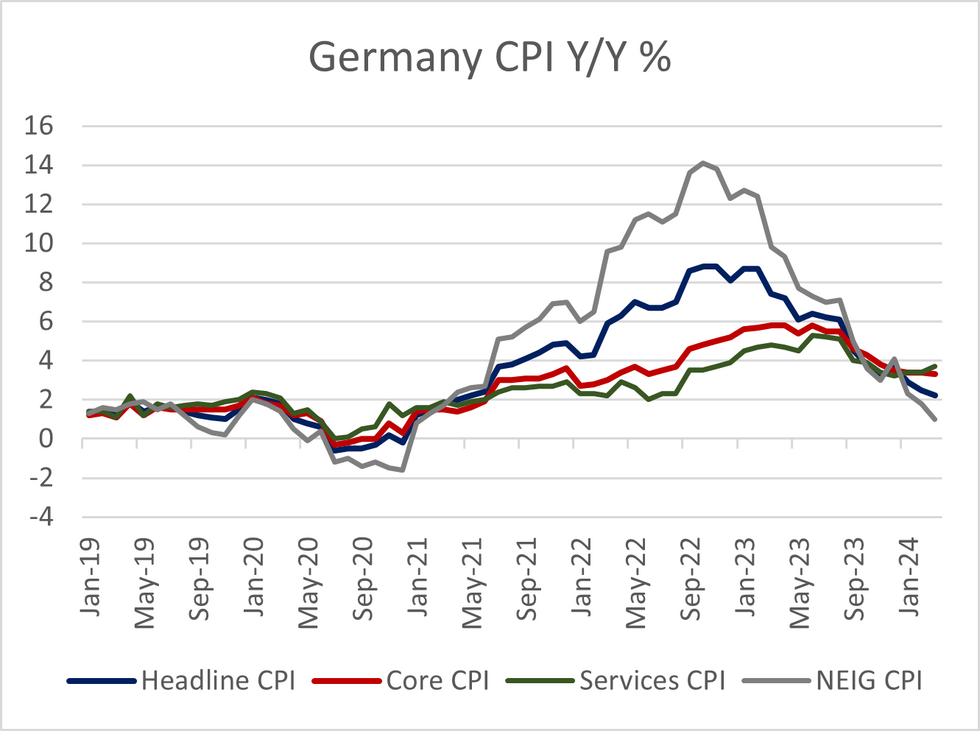

The German national flash March HICP print came in below consensus at 2.3% Y/Y (vs 2.4% cons, 2.7% prior) and 0.6% M/M (vs 0.7% cons, 0.6% prior). The downside surprise was telegraphed somewhat by the state-level CPI this morning.

- Headline, core and major sub-component inflation all fell in line with MNI's tracking estimates based on the state-level data.

- National flash CPI was 2.2% Y/Y (vs 2.2% cons, 2.5% prior) and 0.4% M/M (vs 0.5% cons, 0.4% prior). Core CPI (excluding food and energy) was 3.3% Y/Y (vs 3.4% prior).

- Of the major sub-components, services CPI accelerated to 3.7% Y/Y (vs 3.4% prior), while goods CPI moderated to 1.0% Y/Y (vs 1.8% prior).

- Food CPI decelerated on the back of favourable base effects, at -0.7% Y/Y (vs 0.9% prior), while energy CPI remained in deflation at -2.7% Y/Y (vs -2.4% prior).

- Taken alongside an acceleration in Italian services inflation last week, Eurozone-wide services HICP inflation (released tomorrow at 1000BST/1100CET) may see another month hovering around the 4.0% Y/Y mark (has been exactly 4.0% in each of the previous 4 months).

- This stickiness in services inflation may prompt the ECB at next week's meeting to tone down expectations of a June rate cut.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok