Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

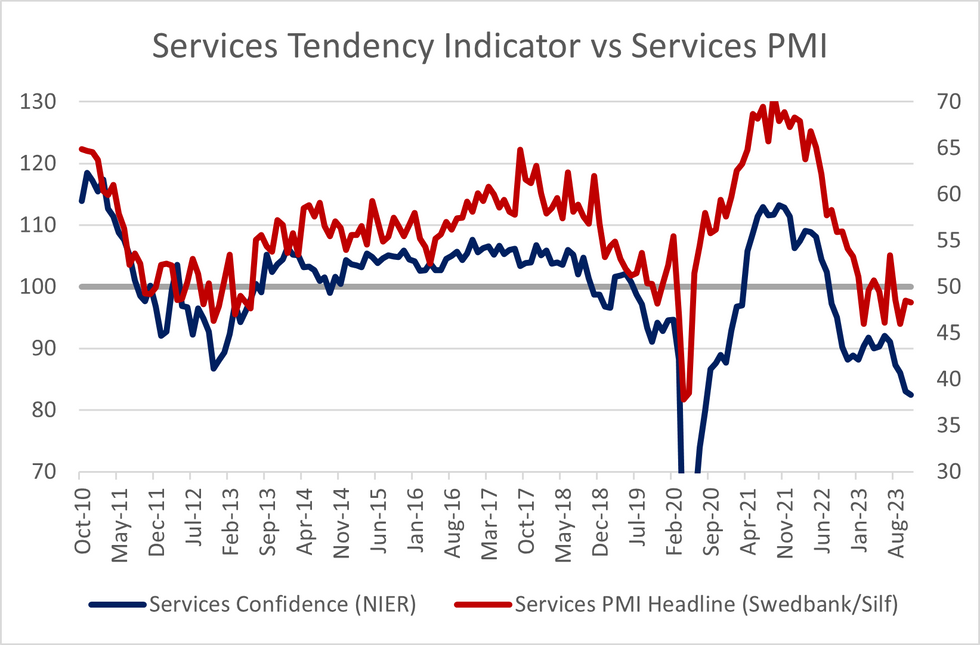

The November services PMI printed a touch lower than October's reading (at 48.3 vs 48.5 prior), remaining in contractionary territory for the fourth consecutive month.

- The index was pulled down by the employment component, which fell to 52.5 from 55.6. There is thus still evidence of some degree of labour hoarding amongst services firms, but momentum is declining.

- The raw-materials/input prices paid component remained at elevated levels, though fell slightly to 59.2 (vs 59.5 prior).

- The development of prices paid and employment are broadly consistent with the November Economic Tendency Indicator, with prices remaining high (albeit off local peaks) and evidence of a softening labour market continuing to be shown in survey data.

- An improvement in supplier delivery times was an upside contributor, while other components showed marginal changes.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok