Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

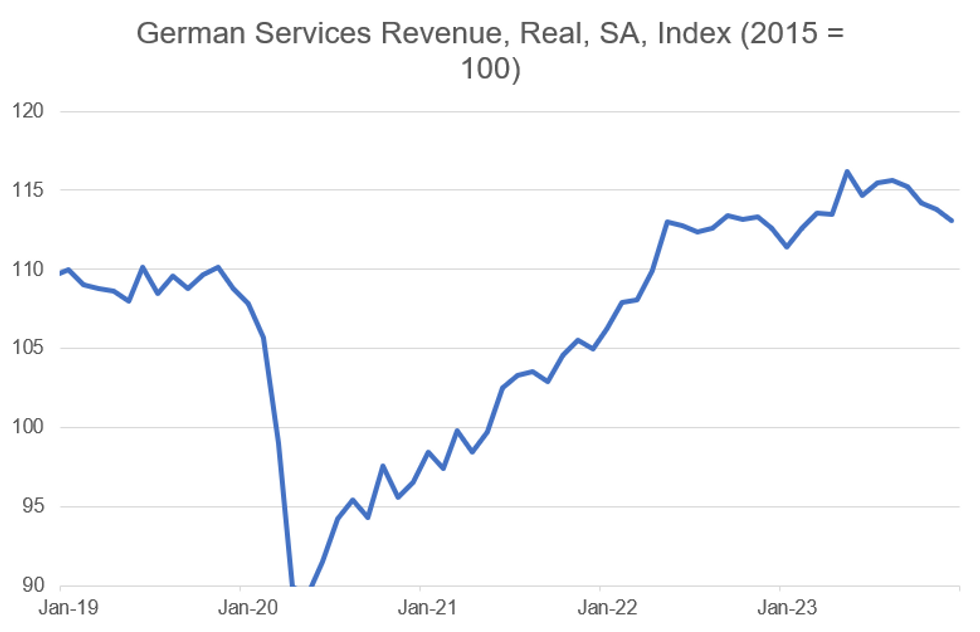

Turnover in German services sectors (excl. finance and insurance) weakened further in December, coming in at -0.6% M/M (vs -0.4% prior). On a yearly comparison, turnover is still up, however, at +0.4% Y/Y (vs +0.4% prior).

- Those figures, which are reported by Destatis in real (inflation adjusted) and seasonally adjusted terms, represent the fourth monthly decline in a row. The 3M/3M measure came in at -1.5% (vs -0.8% prior), the third decline after 6 consecutive positive prints.

- Furthermore, looking at the index level, a downtrend appears to be forming (see the chart below).

- In spite of this weakness through the end of 2023, as a whole, the year printed an all-time high and +2.0% Y/Y (real, but not seasonally- and calendar-adjusted).

- Services had been relatively resilient compared to the manufacturing sector in Germany, but the weakness which started to emerge at the beginning of autumn last year seems to continue with survey data showing little enouragement.

- Activity implied by the German Services PMI has remained in contractionary territory since December, coming in at 48.3 in February (47.7 Jan, 49.3 Dec). The latest release cited "tight financial conditions, client uncertainty and associated weakness in the wider economy (particularly the manufacturing and construction sectors)", with the new business category printing a contraction for the eighth consecutive month. The IFO services subbalance also printed in contractionary territory since mid-2023 (-4.1 Feb, -4.8 Jan).

- Note that services ex financial and insurance accounts for roughly 2/3 of German GVA.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok