Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

Total Fed assets continued to hit new highs last week, closing the week to Wednesday at $7.831trn. Tsy/TIPS made up about 70% of the total $20.2bln increase, with MBS remaining unchanged.

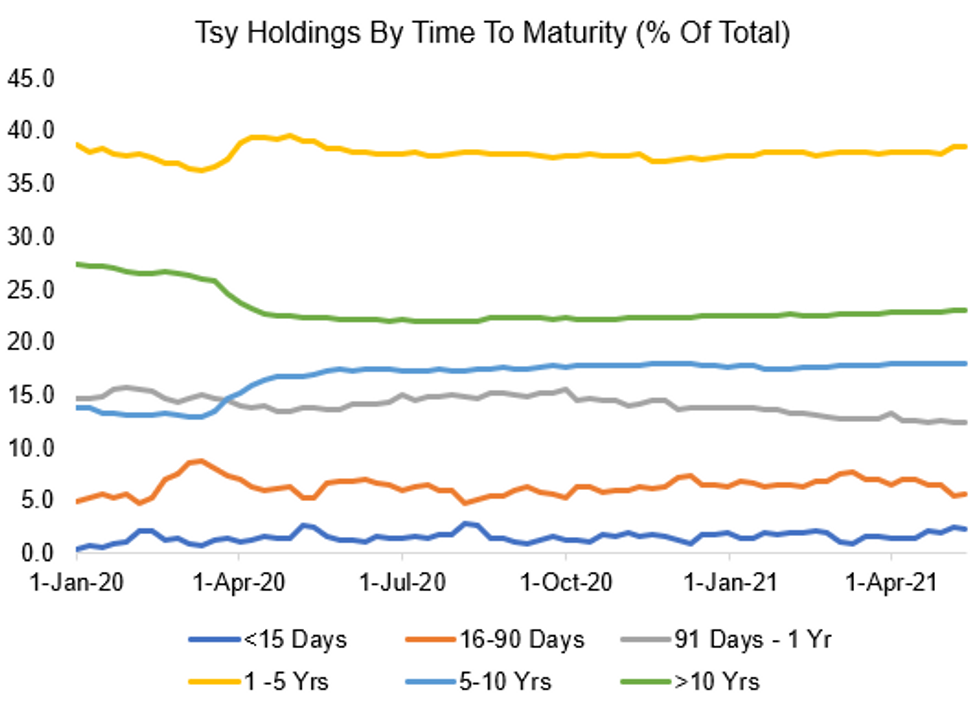

- With much of the interest in Fed purchases last week surrounding a "tweak" in purchase buckets from 10-Yrs onward, it's worth noting that the maturity of holdings has already shifted somewhat this year, albeit at the short end.

- Holdings of securities maturing in <90 days has fallen from a peak of 8.9% of the holdings in Feb to 8.0% currently, while 90 days-1Yr has declined since 4Q 2020 from 15.6% to 12.5%. Most of the difference is attributable to a steady rise in the proportion of 1-5Yr securities, which make up 38.5% of holdings, vs 37.5% in 4Q 2020.

- Total holdings have increased across the spectrum though: increases since Sep 2020 have been $44bn for <1Yr, $275bn for 1-5 Yr, $122bn for 5-10 Yrs, and $168bln for >10Yrs. That said, within that, the 91-day to 1-Yr bucket has seen a $63.8bln decline - likely as securities have drifted closer to their maturity dates.

Federal Resserve

Federal Resserve

| Assets | Total Assets | MBS | TIPS | Treasury Bonds/Notes | Other |

| Last Week's Net Change (USDbn) | 20.2 | 0.0 | 3.6 | 14.0 | 2.6 |

| 4-Week Net Change (USD bn) | 37.6 | -57.7 | 2.5 | 80.9 | 11.9 |

| Total Holdings (USD bn) | 7830.7 | 2191.3 | 339.7 | 5054.4 | 582.6 |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok