Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

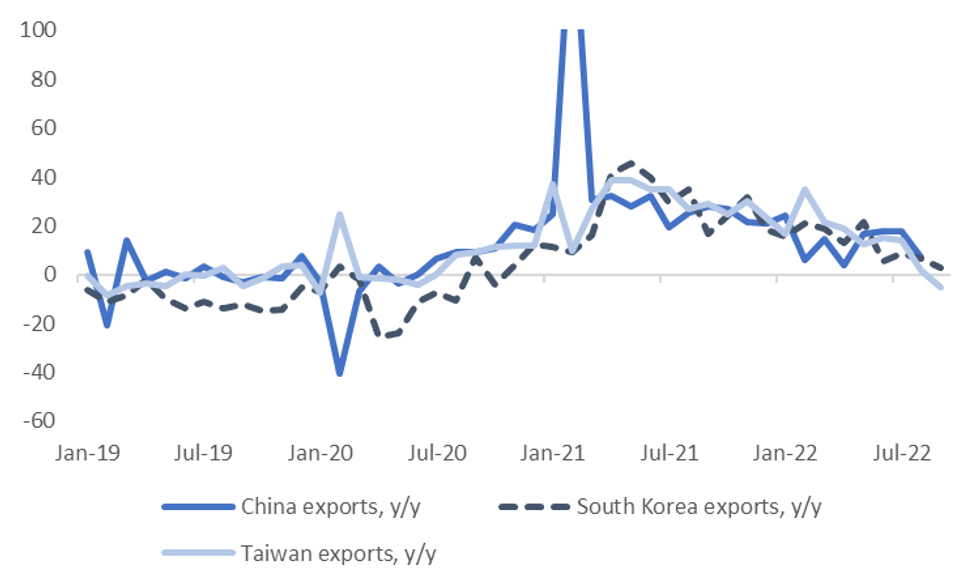

This Friday China trade figures are due. There will be a number of focus points. On the export front (market expects +4.0% y/y, versus 7.1% previously), September prints for South Korea and Taiwan already show a further slowing in external demand. The chart below overlays export growth for these two economies and China. The series are all reasonably correlated with each other, albeit not as strong in recent years, as Covid/supply chain disruptions have generated spikes/slumps in particular months.

- Still, the broad trends tend to follow each other. Taiwan's export update last Friday was particularly soft, falling to -5.3% y/y, well below expectations and the softest pace since early 2020.

- The longer run correlation between Taiwan and China export growth is 36%, slightly higher for South Korea at 41%, although as noted above these are lower in recent years.

- A weaker export picture for China, which has been a source of strength for the country earlier 2022, will put greater emphasis on the domestic recovery, particularly as we progress into 2023.

- Imports are expected to remain close to flat (0.2% y/y expected, versus 0.3% y/y previously).

Fig 1: China, South Korea & Taiwan Export Growth y/y

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok