Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

German final February HICP was unrevised from the flash readings as expected at +2.7% Y/Y (+3.1% Jan) and +0.6% M/M (-0.2% Jan). The final reading of CPI was also unrevised at +2.5% Y/Y (+2.9% Jan) and +0.4% M/M (+0.2% M/M). Core CPI printed at 3.4% M/M (+3.4% Jan). For the monthly headline CPI Y/Y, this represented the lowest value since June 2021.

- The split amont the main December CPI components confirmed the flash reading. Goods prices printed at +1.8% Y/Y (vs +2.3% Jan), services at +3.4% Y/Y (+3.4% Jan).

- Energy continued printing in deflationary territory, at -2.4% Y/Y (vs -2.8% Jan). Looking at the underlying drivers from the subcategories that weren't available in the flash reading: household energy prices decreased 3.6% Y/Y (-3.4% Jan), and fuels deflated 0.4% Y/Y (vs -2.0%

- Food prices, which were one of the main inflation upside drivers in 2023, but disinflated towards the end of the year, saw that trend continue in February, coming in at +0.9% Y/Y (vs +3.8% Jan).

- Within the core measure, specifically core goods, durable goods inflation increased and came in at +2.6% Y/Y (+2.3% Jan); in the details, developments were mixed, used car prices increased +8.7% Y/Y but mobile phones deflated by 5.2% Y/Y. Within services, notable items were rents at +2.2% Y/Y (+2.1% Jan), insurance at +9.8% Y/Y (+10.2% Jan) and package holidays at +9.0% Y/Y (vs +6.5% Jan).

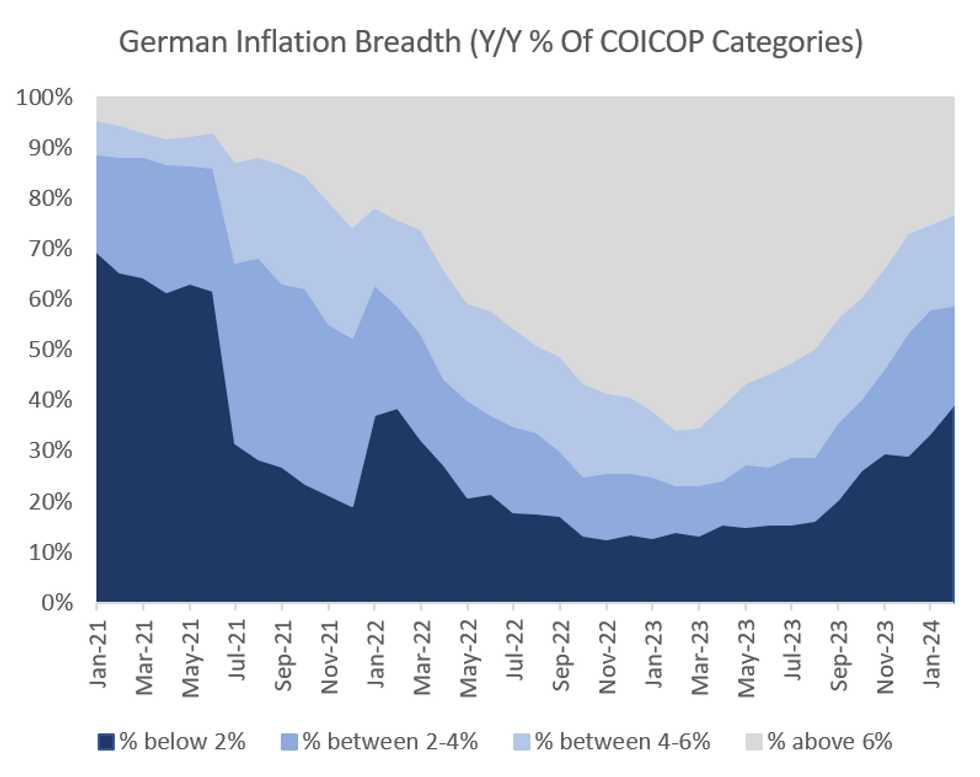

- MNI's HICP inflation breadth indicator (see chart below) shows disinflation progresssing for items which already saw low-to-medium inflation recently, as the percentage of categories printing below 2% increased to 39.1%, up from 33.6%. The percentage of categories printing at or above 6% also decresed, to 23.2%, down from 25.1% in December - the pace is slowing here, however.

- The key piece to observe the coming inflation releases will continue to be services - after the stall in its yearly rate, service inflation is considered to be a main obstacle to an ECB rate cut.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok