Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

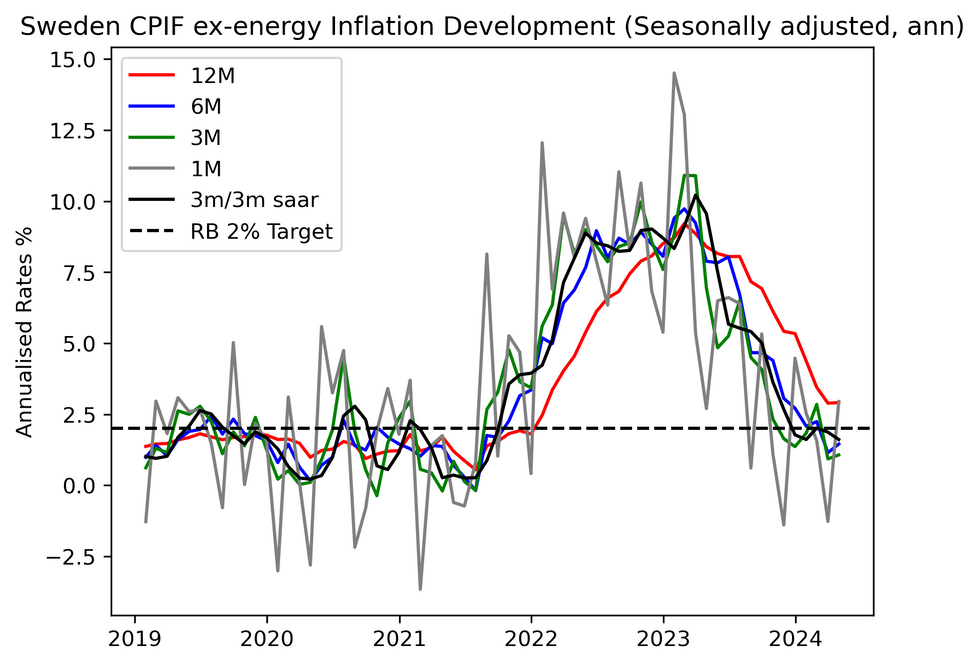

Swedish April CPIF ex-energy printed 2.9% Y/Y at (vs 3.0% cons, 2.9% prior). The Riksbank had projected a reading of 3.3% Y/Y in the March MPR, meaning the rounded forecast error of those projections remains steady at -0.4pp.

- MNI’s estimate of seasonally CPIF ex-energy printed 2.9% Y/Y at (vs 3.0% cons, 2.9% prior). The Riksbank had projected a reading of 3.3% Y/Y in the March MPR, meaning the rounded forecast error of those projections remains steady at -0.4ppadjusted inflation indicates that CPIF ex-energy rose 0.24% M/M in April, while inflation momentum at different time horizons increased slightly.

- Headline CPIF was also below consensus at 2.3% Y/Y (vs 2.4% cons, 2.2% prior and 2.7% Riksbank).

- We still don’t think this changes the picture much re: a possible June cut, given we will receive another inflation reading before the June meeting and the Riksbank’s guidance suggests the bar to cut in consecutive meetings is already quite high.

- SEK is biased a touch weaker following the release, but moves have been very modest.

- Looking at the sub-categories, the housing, electricity, gas and other fuels category moderated to 8.6% Y/Y (vs 9.3% prior), with a moderate increase in rents not enough to offset the M/M deflation in electricity prices. These dynamics were as expected.

- Core categories also appear mixed: Restaurant and hotel inflation rose to 5.6% Y/Y (vs 4.0% prior), with health and communications also seeing higher Y/Y readings vs March. On the other hand, recreation and culture continued moderating to 2.4% Y/Y (vs 3.1% prior).

- Clothing and footwear moderated in April, while furnishings and household equipment was -0.2% Y/Y (vs -0.7% prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok