Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

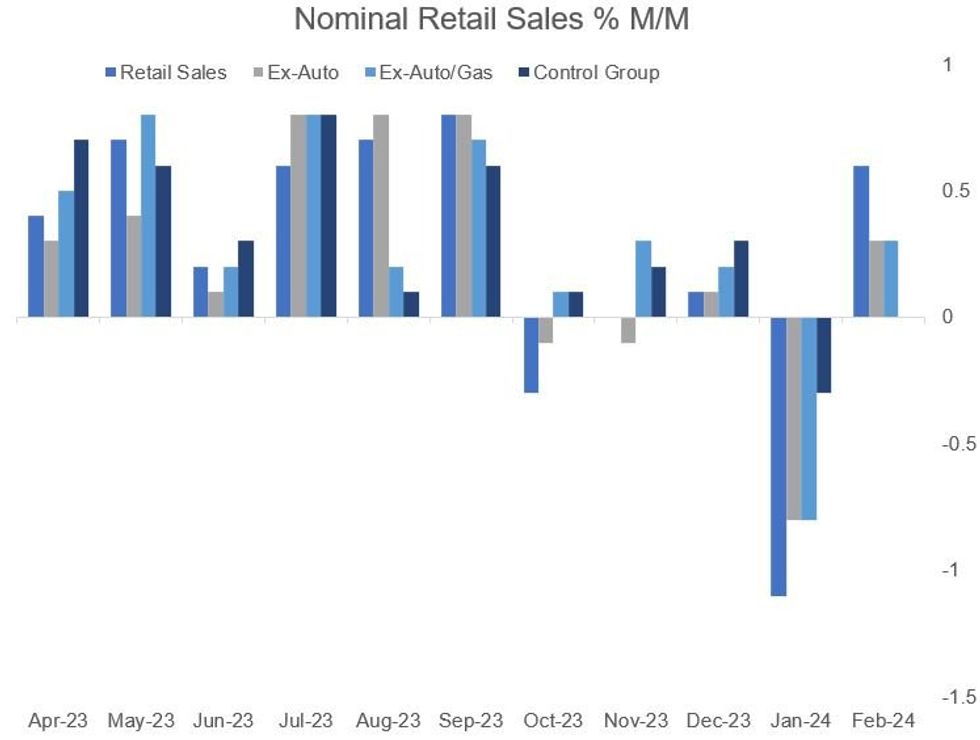

US retail sales printed on the weak side in February across headline and core measures in the advance estimate, compounded by downward revisions to January's figures.

- Overall retail sales rose 0.6% M/M (vs 0.8% survey, -1.1% prior reflecting downward revision by 0.3pp), with ex-auto/gas sales up 0.3% (in line with expectations, but prior -0.8% including -0.3pp revision).

- The GDP input Control Group saw flat growth versus expectations of +0.4%, though January's reading was upwardly revised 0.1pp to -0.3%.

- While retail sales rebounded from a weak January, the downward revisions ensured nominal sales in February remained below September 2023 levels - while "real" (CPI-deflated) sales have flatlined in the first 2 months of 2024 at levels last seen in Q2 2023.

- There were few standouts among retail sales categories, with improvements potentially reflecting both better weather in February vs January, and some upward inflationary effects (particularly for gasoline). Motor vehicle/parts dealer sales rose 1.6% (-2.1% prior), with building material sales up 2.2% (partly reversing January's sharp -4.3% drop), while gas stations posted a 0.9% rise (-1.4% prior).

- Food services/drinking places saw 0.4% growth after -1.0% in January, with food and beverage store sales up 0.1% after -0.3% prior.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok