Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

The flash readings of Eurozone inflation came in at/slightly above consensus estimates coming into the week, but were mostly in line with the expectations formed after national-level prints received prior. All in all, core pressures remain uncomfortably high, but appear to be settling down to a sequential pace that is closer to 2% than to the 4-5% suggested by prints earlier in the year.

- Headline HICP printed at 5.3% Y/Y (5.26% unrounded, 5.3% Jul), and 0.6% M/M (0.56% unrounded, -0.1% July). Those were above the 5.1% / 0.4% consensus but accorded with MNI's estimates based on earlier national prints.

- Likewise the 5.3% Y/Y core HICP reading (5.29% unrounded, 5.5% Jul) with core at 0.3%% (0.34% M/M unrounded) were in line with MNI's expectation coming into the reading, and matched previous expectations - potentially reflecting marginal upside surprises to German and Spanish core, with softer French and Italian readings offsetting.

- On the headline front: energy prices rose 3.2% M/M, bringing the Y/Y rate to -3.3% from -6.1% in July, as various base effects reversed and oil prices rose. Unprocessed food prices fell 0.6% M/M, with procesed food/alcohol/tobacco up 0.3% - both Y/Y figures moderated (processed 10.4% vs 11.3% prior; unprocessed 7.8% vs 9.2% prior).

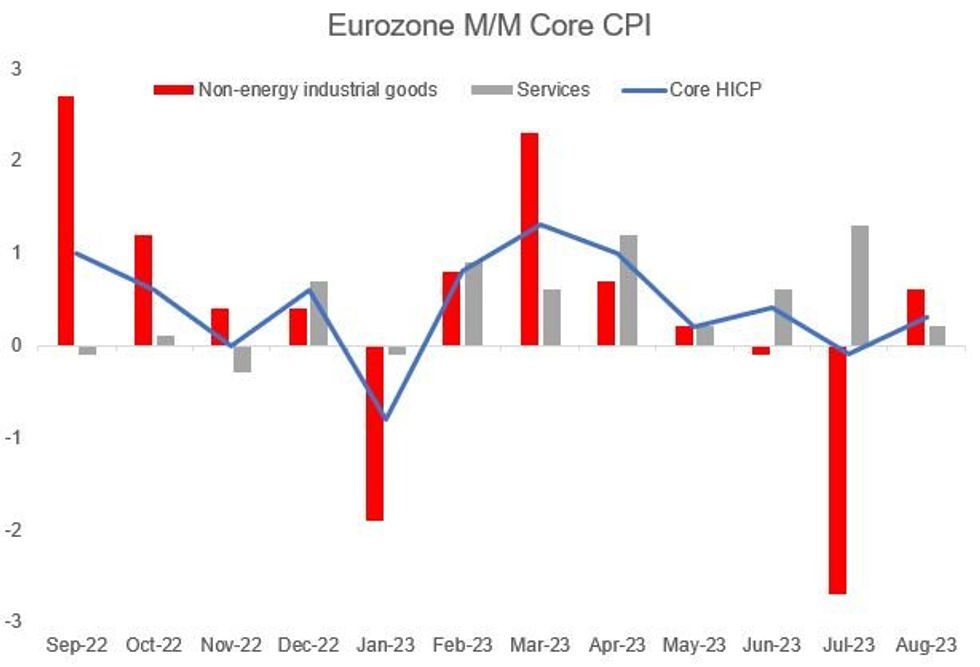

- As for core items, non-energy industrial goods prices continued deflating Y/Y, to 4.8% (5.0% prior), with services likewise a touch lower (5.5% vs 5.6% prior).

- While sequential NEIG deflation in the prior 2 months (incl -2.7% M/M in Jul) reversed to inflation (+0.6% M/M Aug), part of this may be due to effects of shifting sales periods.

- Additionally, services rose just 0.2% M/M - joint-lowest since January - vs 1.3% in July. The latter was boosted by statistical factors that should fade going forward. Indeed some had expected services would mark another Y/Y high in August before an inevitable fading in September onward - this report marked a positive development on the disinflation front in that regard.

Source: Eurostat, MNI

Source: Eurostat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok