Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

MNI (London)

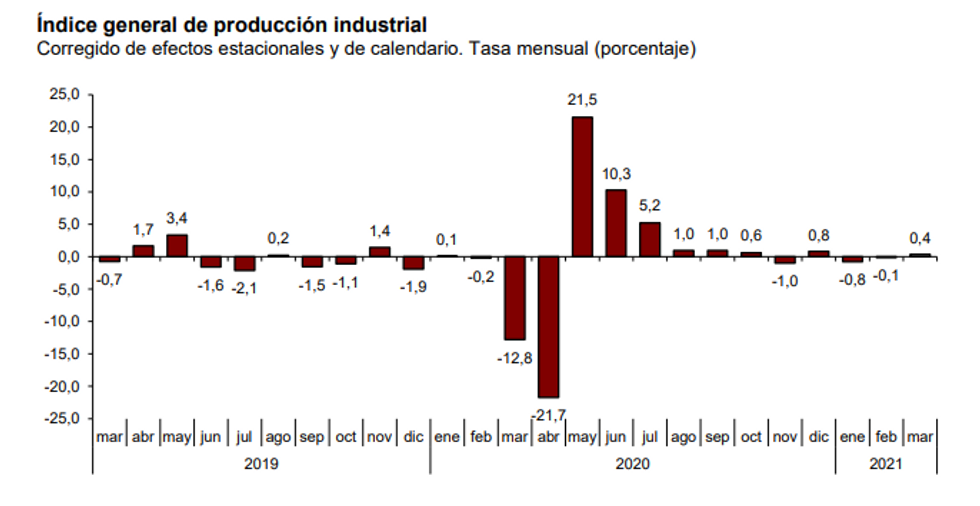

SPAIN MAR IND PRD +0.4% M/M, +12.4% Y/Y; FEB -0.1% M/M

- Spanish IP rebounded to 0.4%, slightly short of market expectations of a 0.5% uptick.

- Feb's reading was revised down to -0.1% from 0.0% reported previously.

- Annual production surged to 12.4% in Mar, reflecting base effects due to the sharp decline at the beginning of the crisis.

- Mar's uptick was led by a 1.1% increase in consumer non-durable goods output, followed by durable consumer goods output rising by 0.7% on a monthly basis.

- Intermediate goods output edged up 0.4% in Mar, while energy output was flat.

- Capital goods production saw the only decline among the main categories, falling by 0.4% in Mar.

- The clothing and textile industries saw the largest monthly gains, rising by 19.9% and 13.6%, respectively.

- On the other hand, tobacco production recorded the larges drop, down 11.7% m/m.

Source: Ine

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok