Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

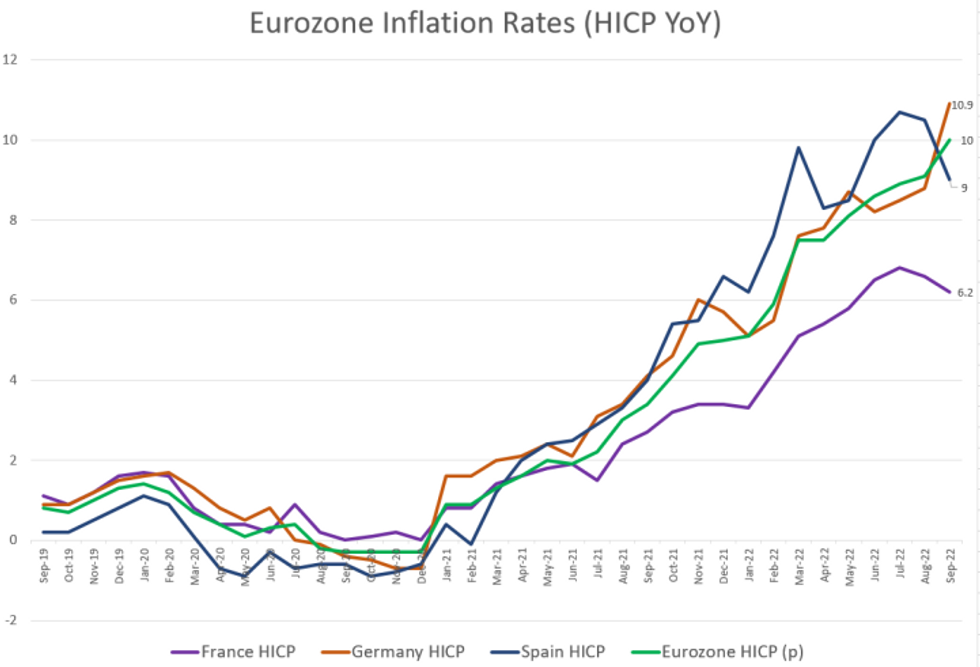

FRANCE FINAL SEP HICP -0.5% M/M, +6.2% Y/Y (FLASH CONFIRMED)

SPAIN FINAL SEP HICP -0.2%r M/M (FLASH 0.0%), +9.0%r Y/Y (FLASH +9.3%)

- French HICP in September was confirmed to have fallen by 0.5% m/m (vs +0.5% in Aug) and decelerated for the second consecutive month to +6.2% y/y (vs +6.6% in Aug, +6.8% peak in July).

- Compared to August, French prices are seeing a broad-based slowdown lead by energy prices. Service prices contracted by 1.5% m/m due to a marked seasonal decline in tourism and manufactured products and food price inflation slowed.

- Spanish HICP saw downwards revisions to final September prints, by 0.2pp to -0.2% m/m and by 0.3pp to +9.0% y/y. This is also the second month of slowing headline inflation following the July peak of 10.7% y/y.

- Housing and transport saw significant year-on-year price deceleration due to falling energy and fuel prices.

- French and Spanish core inflation prints saw September relief, stepping down by 0.2pp to 4.5% y/y and 6.2% y/y respectively.

- The eurozone aggregate final CPI is due on Wednesday, having hit 10% in the flash. As such, this data provides little relief for the ECB as significant upwards pressure comes from other parts of the bloc. As such, the ECB still has another 75bp hike for the Oct 27 meeting in sight.

Source: MNI / Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok