Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CZECHIA

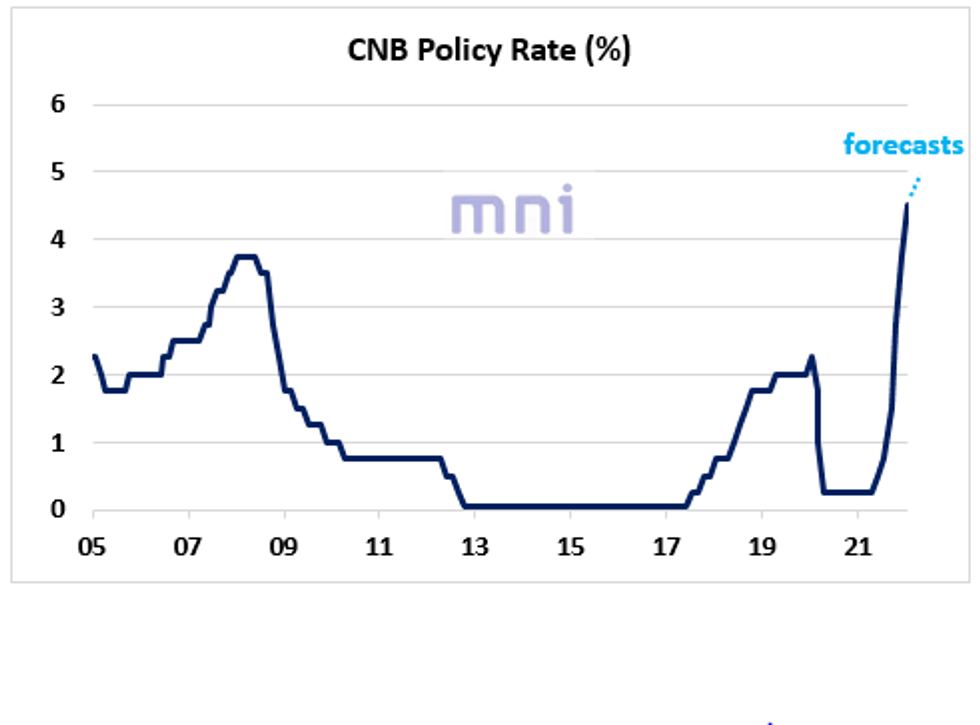

- Last week, the minutes of the CNB February meeting showed that some policymakers see Czech rates remaining elevated for longer than previously estimated given the current inflationary pressures.

- This morning, economic data showed that Czech inflation accelerated to 9.9% in January (vs. 9.3% exp.), up from 6.6% the previous month and currently standing at its higher level since July 98.

- We saw that the CNB has now entered into the last phase of the tightening cycle, with the terminal rate expected to reach 5% in the near term.

- Given the high inflation print, the CNB is likely to proceed with another ‘big’ 50bps hike in the March meetings (31st); some sell-side firms are expecting two 25bps hikes in March and May.

- The terminal rate, which is now standing above Czech so-called ‘neutral’ rate, was expecting to gradually decline from H2 2022 (slowly converge towards the neutral rate) as inflation starts to decelerate.

- However, the persistent of inflation could delay the ‘easing cycle’ for late 2022 early 2023.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok