Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

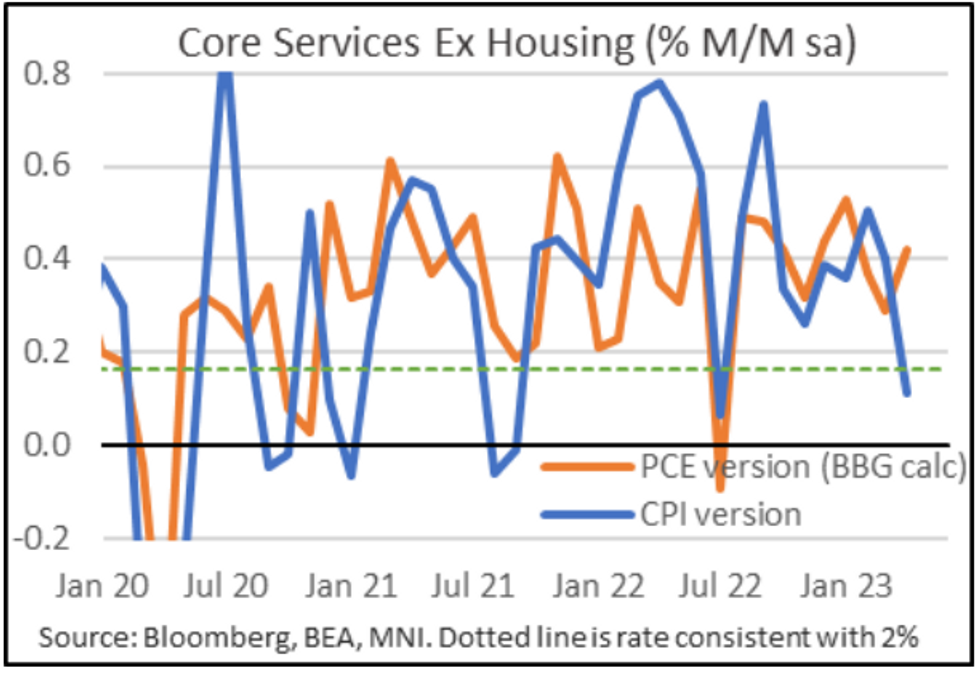

Today's US inflation report for May presents a clear risk to Wednesday's FOMC decision and communications - and mostly in a hawkish direction if (as expected) the Fed came into today planning on delivering a hold.

- Our view is that the bar to a hike has been set very high and it would require a significant beat on CPI to seriously put a raise on the table. (Our CPI preview is here.)

- With consensus on core at 0.4% M/M (with a downside skew in the survey w average at 0.36%), the figure would either have to be 0.5% M/M to begin having that conversation, or in the case of an in-line reading, for the details themselves to be relatively worrisome.

- Note that the last two monthly core readings were in line and saw yields drop sharply.

- It would probably require both a beat and worrying details for serious consideration of a surprise hike Wednesday. Particular attention will be paid to the role paid by rents: if we get a strong core figure, and it's driven mostly by shelter, the FOMC will largely look through it as it is more focused on services ex-housing. In terms of expectations: OER seen at an average 0.50% (range 0.46-0.54%) and primary rents an average 0.53% (range 0.48-0.60%). We'd also put used cars in this category, as they are are seen pulling back in May. If it's ex-cars, ex-shelter driving the beat, that will be considered relatively worrisome for the FOMC.

- Ex-Fed Vice Chair Alan Blinder (who argues for no further Fed hikes) told MNI last week that a "really bad looking" CPI report could still prompt a surprise 25bp hike, with Chair Powell "right in the middle" of the increasingly divisive hawkish and dovish factions.

- Though with the bar to a hike set so high by pre-blackout communications, an unexpectedly hawkish CPI report today could instead translate into a more aggressive dot plot (more members seeing potential for 2+ further hikes this year to above the 5.4% median that is consensus for the June dot plot) in conjunction with an increased core PCE forecast for 2023 (already seen rising from 3.6% in March to 3.7-3.9%). It would probably tilt Powell's press conference more hawkish too.

- It could also cement some hawkish dissents. The prime candidates among voting participants are Kashkari and Logan; Bowman and Waller might object but there hasn't been a Governor dissent in nearly 20 years.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok