Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS/SUPPLY

All analysts whose post-Refunding reactions we have seen have (unsurprisingly) raised their outlooks for Treasury supply amounts over the coming year. Roughly speaking, the expected peak pace of issuance (occurring either in the May or Aug 2024 Refunding month) are around $20B higher vs pre-Refunding expectations.

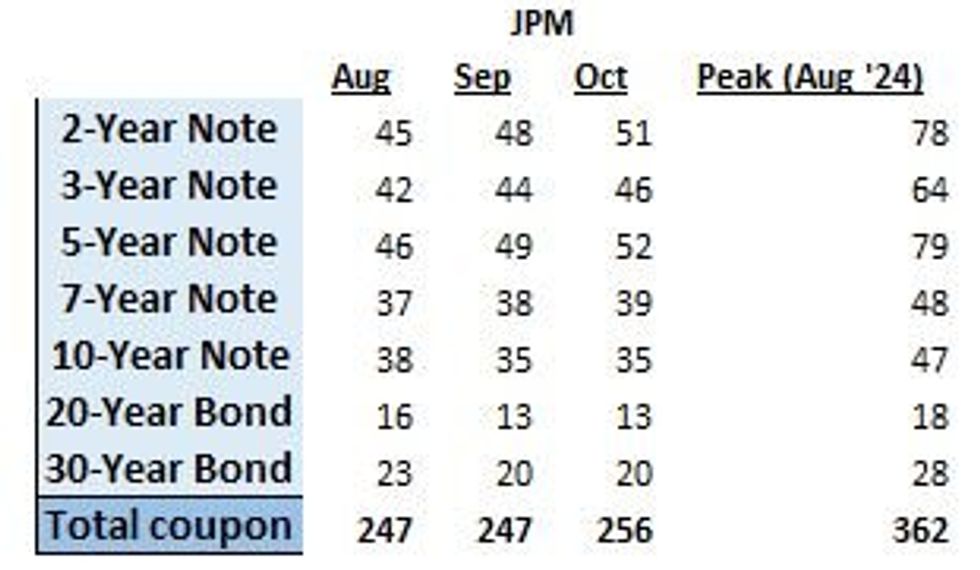

- JPM now sees supply rising over the coming year and peaking in Aug 2024 at $362B - that compares with $247B this August and includes (see image) increases in 2Y note to $78B (from $45B projected by Tsy for Aug 2023), in 3Y to $64B (from $42B), in 5Y to $79B (from $46B), in 7Y to $48B (from $36B), in 10Y to $47B (from $38B), in 20Y to $18B (from $16B), and in 30Y to $28B (from $23B).

- In our Refunding Preview, JPM had the highest published forecast we'd seen for peak monthly issuance sizes, at $340B, but even this had to be raised by $22B after Wednesday's announcement.

- As for Bills, JPM sees net issuance $1.815T this year (vs $1.077T coupons) but moving into 2024 coupons will retake the lead ($2.234T vs $0.198T), bringing bills' share of debt back down to 20%.

- "Like our prior forecasts, with budget deficits already sitting at a larger share of GDP than prior cycles, and the Fed’s QT process likely to continue even after the Fed begins easing, we think Treasury will announce similar-sized increases at the coming 3 refundings."

Note: JPM's 7Y Note forecast is $1B higher than Treasury's for Aug/Sep/OctSource: JPMorgan

Note: JPM's 7Y Note forecast is $1B higher than Treasury's for Aug/Sep/OctSource: JPMorgan

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok