Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

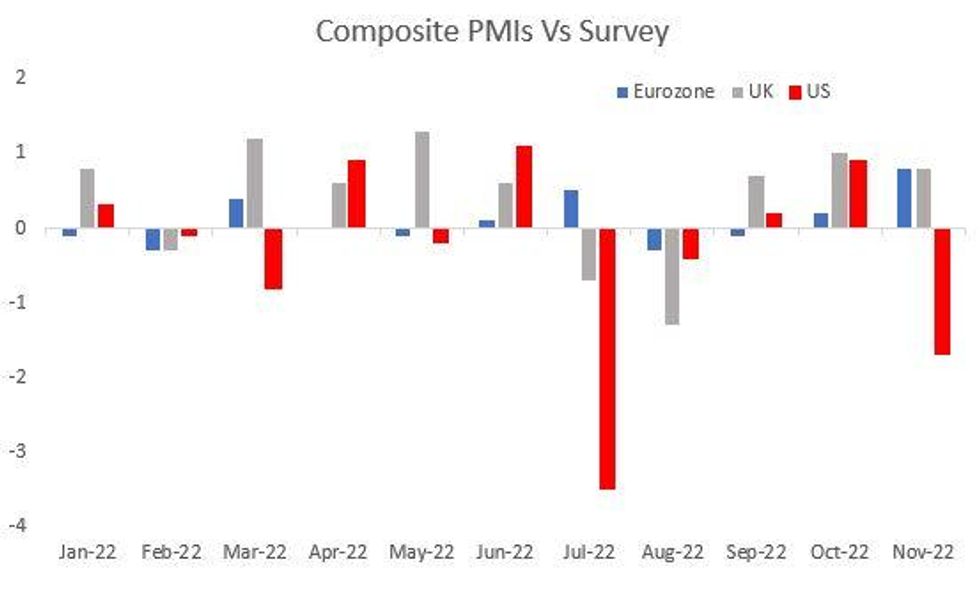

Data out this week, primarily the Nov prelim European and US PMI readings out Wednesday, varied slightly in composition and in direction of surprises. But it carried a common theme: activity and employment are slowing, and price pressures are showing more signs of pulling back as demand cools.

- Europe's readings were for the most part above-expected, including PMIs and German IFO confidence. The composite eurozone PMI figure is clearly recessionary. But that was to be expected, with the energy price shock making the (likely) current recession one of the most widely anticipated ever.

- In this context, the the widely-expected eurozone recession may not be as bad as feared. Forward-looking indicators were poor, but the decline into contraction so far has been fairly steady, and doesn't appear to be accelerating. Eurozone factory output fell for a 6th consecutive month, but the rate of decline has eased. The decline in services PMI was unchanged.

- Similarly, UK readings were likewise recessionary, but PMIs "beat" vs expectations amid unchanged declines across manufacturing and services.

- The US PMIs were weak and missed by the most since July. But that previous miss proved an outlier and subsequent data dispelled concerns of a broader stall in the economy.

Source: S&P Global, BBG, MNI

Source: S&P Global, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok