Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

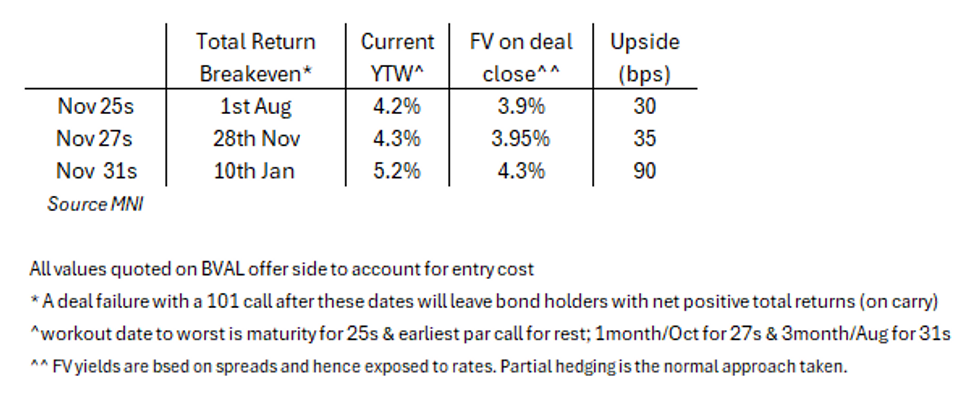

- Citi with some optimistic takes that Capri deal closing is still the "very realistic scenario", see here. A welcome view for TPR longs but we wouldn't read-through too much into it given 1) market analyst have been lagging the share px slide (the FTC block had street rumours leak before it happened) and it has not recovered since and 2) we have seen some heavy cuts to deal not closing since, including Jefferies (from $57 to $38).

- Adding to that the risk-reward for credit has gotten tad worse since we last looked at it (see below) on decaying carry protection. That's not helped by recent renewal in rates vol - a issue given the nuance around hedging to account for FV into spreads but also remain exposed to px moves.

- Upside still sizeable on longer 31s for those that have FIRM bias to deal closing - though investors should compare that risk-reward to CPRI equities which have +78% upside.

- Citi is in range of what most M&A arb. analysts and we have assumed on deal failure for CPRI share px; that it will revert to trading at a P/E multiple close to pre-deal announcement between c$20-25. Based on that we see equity markets pricing 65%-75% prob. of failure.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok