Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

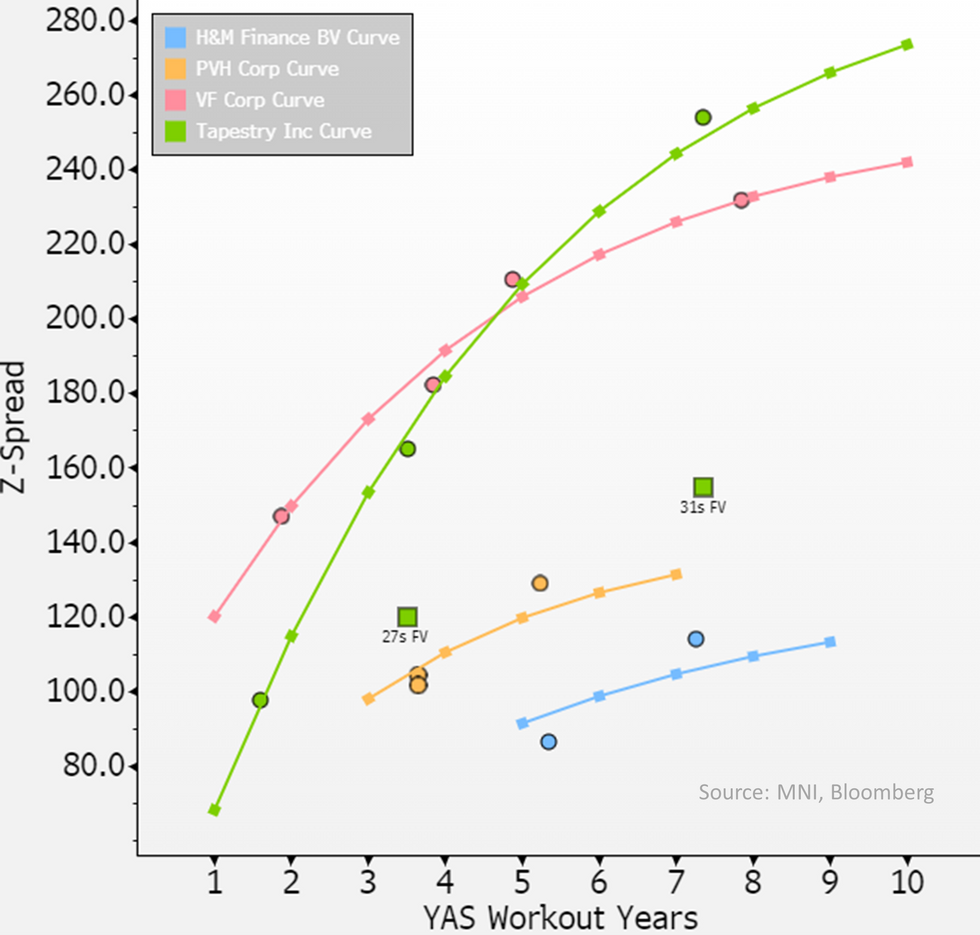

- Slight change to earlier screen on 27's; 31's still have ~double upside on deal closing (~100bps of tightening) & despite breakeven coming down to September (vs. July on 27s), given FTC docs' have 25th September as date of hearing downside risk may be limited and still benefit 31s....uncertain if co's will push for expedited pace (which it would likely prefer) - FTC doc's don't indicate that as a possibility to us.

- If cash prices between the two move to same price (as they were earlier last week around ~€102) gives 'risk-less' opportunities for flatteners.

- For those looking to trade a deal not closing view, Capri equities and/or $33's (at $104.5) may be better expressions - though both were resilient after the headlines yesterday.

Note lines benefit from 25bps per agency per notch (Moody's and S&P) below Baa3/BBB- coupon step-ups up to a maximum of 200bps. As we said we expect downgrade to Baa3 on deal closing, some protection there for long-end lines if integration struggles. Deal not closing not shown below, please note breakevens mentioned don't include any funding costs.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok