Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UTILITIES

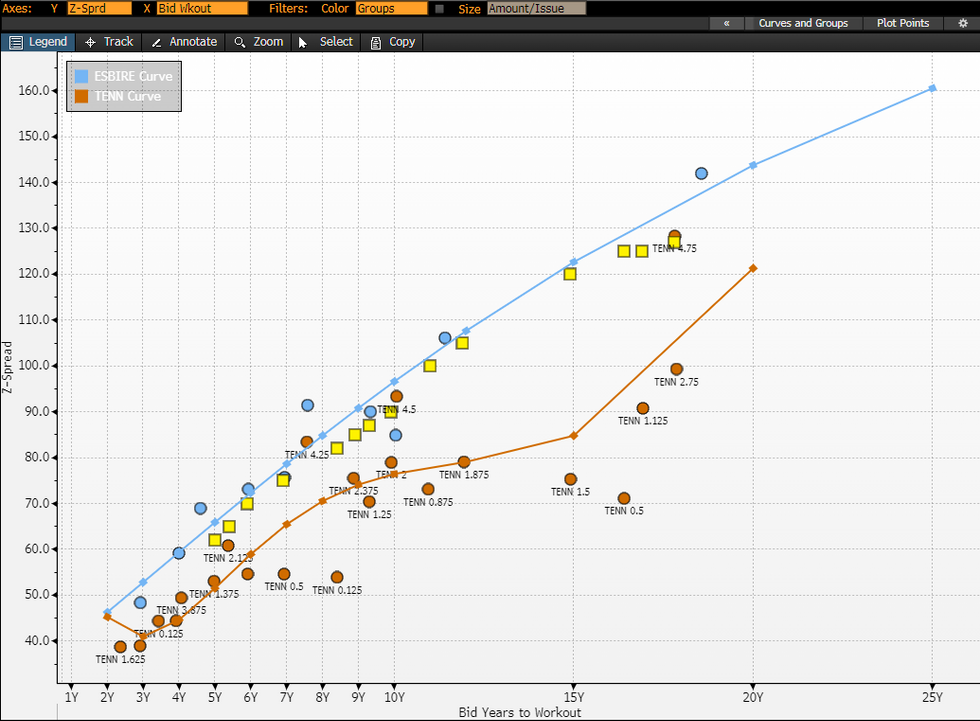

- Following the recent major repricing of TenneT bonds we revisit what’s priced in on the curve currently.

- To recap: talks between the German and Dutch governments regarding the sale of TenneT’s Germany grid assets fell through due to budgetary constraints. The market had been pricing in a substantial probability of a par takeout due to the wording of a default clause triggered by asset sales. The implied probability was well over 50% before talks collapsed.

- To calculate we must assume a spread in the absence of optionality (yellow on the chart). For simplicity we use ESBIRE (A3/A-) whose curve trades close to the above par TENN bonds.

- We ignore timing for simplicity; implied probabilities would be higher if accounted for due to the opportunity cost of holding tighter bonds. Longer dated bonds have higher implied probabilities due to longer time values.

- Given the assumptions required, we think the exercise is most interesting comparing between bonds.

- On that basis, for investors looking to retain optionality there appears to be value in owning TENN 1.125 41 rather than TENN 2.75 42 and TENN 1.5 39. See the table for probabilities across the curve.

DES Implied P TENN 1 5/8 11/17/26 3% TENN 1 3/4 06/04/27 9% TENN 0 1/8 12/09/27 3% TENN 1 3/8 06/05/28 6% TENN 1 3/8 06/26/29 8% TENN 2 1/8 11/17/29 7% TENN 0 7/8 06/03/30 7% TENN 0 1/2 06/09/31 8% TENN 0 1/8 11/30/32 9% TENN 2 3/8 05/17/33 9% TENN 1 1/4 10/24/33 9% TENN 2 06/05/34 10% TENN 0 7/8 06/16/35 10% TENN 1 7/8 06/13/36 16% TENN 1 1/2 06/03/39 18% TENN 0 1/2 11/30/40 14% TENN 1 1/8 06/09/41 11% TENN 2 3/4 05/17/42 21%

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok