Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EURIBOR

Late on Friday Goldman Sachs noted that “on face value, the ECB meeting was much more hawkish than we expected. But we do think that Lagarde outlined an informal easing bias during the press conference that continues to point to further easing.”

- “There were also hints that projection meetings allows for sufficient data accumulation for further policy adjustment, and so we continue to think that a quarterly pace of cuts is the right baseline.”

- “With markets pricing 33bp to year-end, we think yields will struggle to rise from current levels, and that the hawkish formal guidance lowers the bar for upcoming ECB speak to rebalance the debate a little more dovishly.”

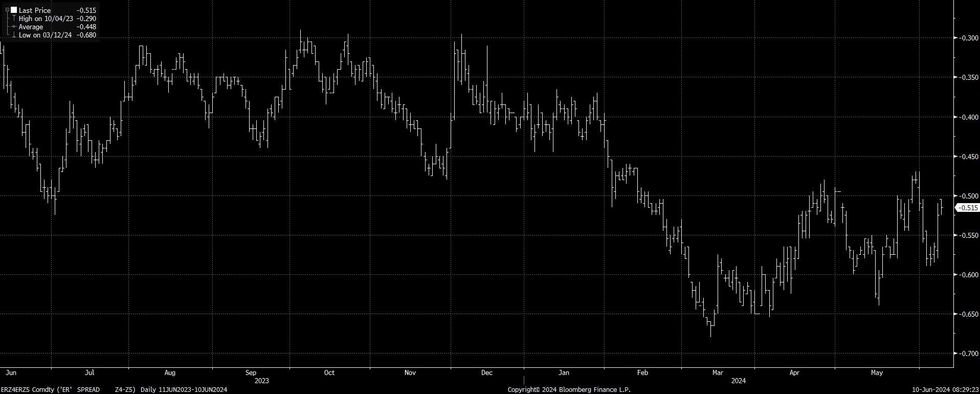

- “But with a long wait until definitive data on a September cut, we expect incremental domestic data and possibly US spillovers to catalyse more curve flattening – we recommend ERZ4Z5 flatteners (at -52.5bp, targeting -75bp, stop -40bp).”

Fig. 1: Euribor Z4/Z5 Spread

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok