Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BONDS

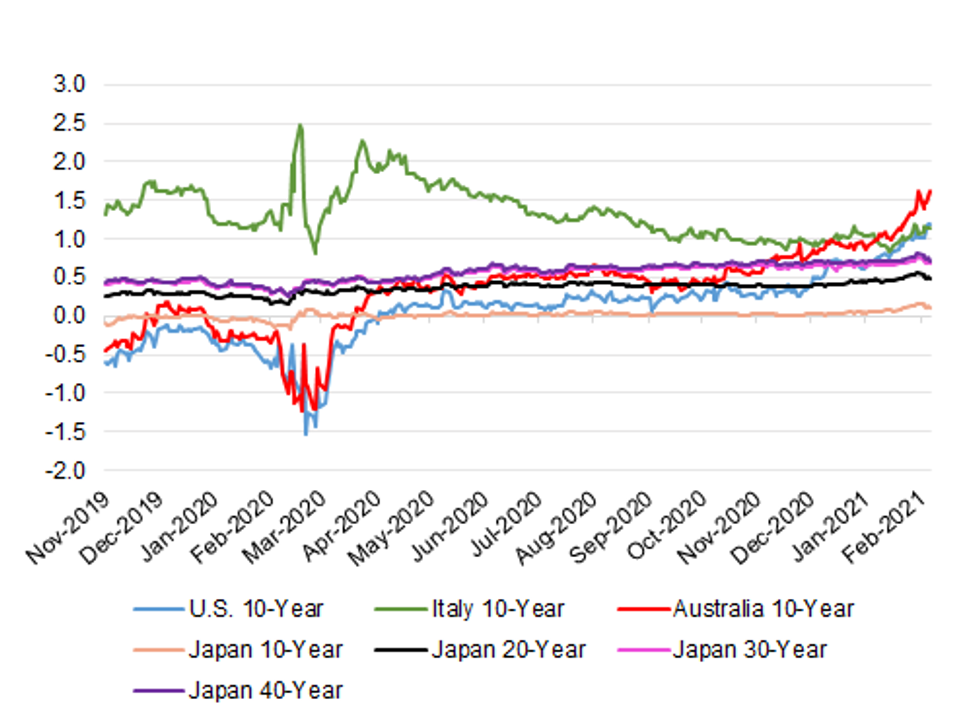

A quick overview of the recent evolution of FX-hedged yields from the perspective of Japanese investors (based on rolling 3-month hedge costs) provides several points of note:

- The recent global curve steepening continues to provide a more attractive FX-hedged yield environment for Japanese investors at least on face value, although the recent bout of volatility in core global fixed income markets, coupled with the proximity to the Japanese FY end, has resulted in the most sizable 2-week round of Japanese net selling of foreign bonds on record (through 26 February), as we have previously flagged. The proximity to Japanese FY end has the potential to undermine Japanese participation until late March/early April, although large bank/fund allocations have been observed ahead of the end of the FY in recent years

- Questions over the sustainability of RBA monetary policy settings and the high beta status of ACGBs have combined to provide particularly attractive entry points for Japanese investors re: ACGBs, although the aforementioned volatility may have resulted in participants taking some money off of the table. Still, many sell-side participants continue point to the habits of Japanese investors in Australia re: a preference for FX-unhedged positions, which provides a further layer of complexity to the argument, with the recent uptick in AUD/JPY providing some insulation for already established longs.

- 10-Year U.S. Tsy yields provide the second most attractive FX-hedged yield entry point within the markets we have flagged, although the lack of outright pushback from the Federal Reserve re: the recent run higher in U.S. Tsy yields, combined with the sizeable U.S. fiscal impulse and the global reflation dynamic provides further points of caution for Japanese investors re: engaging in longs.

- Note that the following levels represent closing levels on 5 March 2021.

| FX-Hedged Yield (%) | Conventional Yield (%) | |

| U.S. 10-Year | 1.1829 | 1.5661 |

| Germany 10-Year | 0.0839 | -0.303 |

| France 10-Year | 0.3376 | -0.05 |

| Italy 10-Year | 1.1397 | 0.754 |

| Spain 10-Year | 0.7788 | 0.391 |

| UK 10-Year | 0.5004 | 0.756 |

| Australia 10-Year | 1.629 | 1.8338 |

| Japan 10-Year | -- | 0.096 |

| Japan 20-Year | -- | 0.479 |

| Japan 30-Year | -- | 0.68 |

| Japan 40-Year | -- | 0.716 |

Fig. 1: Selected FX-Hedged Yields From The Perspective Of A Japanese Investors vs. Longer Dated JGB Yields (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok