Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

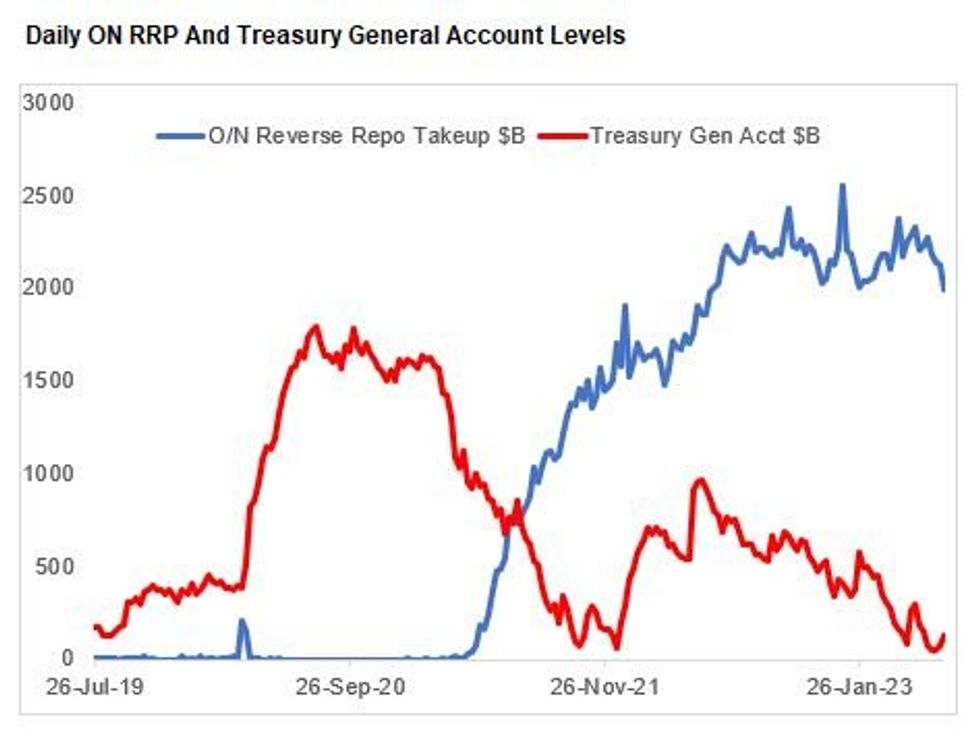

While the decline in ON RRP usage looks likely to continue, it's still too early to determine whether the Treasury's cash rebuild will drag down system reserves to "scarce" levels.

- Note in the week to Wednesday, system reserves were unchanged, and were actually up $26B to $3.306B over the prior 4 weeks despite continued QT (SOMA assets fell a net $52B over the same period), ON RRP fell by $161B and the TGA rose by $66B.

- Those trends are unlikely to be sustained - reserves are almost certain to head lower, to below $3T in the coming months as the TGA is refilled via funds flowing from both banks and money market funds parked at RRP.

- As we discussed in this month's Treasury Issuance Deep Dive (PDF Link here), the “minimum” level of reserves is probably somewhere between $2.3-2.8T, so being conservative, a drain of $400-500B of reserves from current levels could begin to pressure the banking system, if not before. The longer we go on, the more QT will continue to put consistent pressure on the banking system as well.

- Though Fed Chair Powell at Wednesday's press conference was unconcerned with the reserves outlook, It's not hard to see a situation in which reserves fall to $2.9T – the upper bound of the scarcity zone – by end-September.

- And as we get closer to that time, there will be a regular reassessment of whether ON RRP has indeed made up the bulk of bill funding, and whether banks are feeling any pressure.

- As we discuss in the Deep Dive, we'll be looking at multiple indicators on that front in the months ahead, including: bank deposit rates on offer, repo rates, Fed funding facility usage (including BTFP), and borrowing from FHLBs.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok