Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

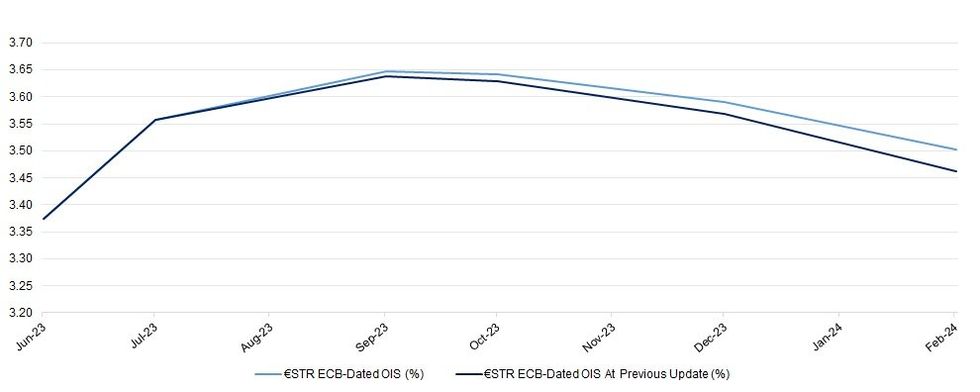

Fairly sticky ECB-dated OIS pricing was evident in the European morning, with meaningful catalysts lacking, leaving participants to brush over the virtually in line with flash final round of Eurozone inflation data for April and ECB’s de Cos sticking to the dovish side of the spectrum.

- Since then, feedthrough from U.S. markets has seemingly allowed some light firming to creep into the contracts covering the Bank’s Sep ’23 to Feb ’24 gatherings. That leaves 17-18bp of cuts priced in between peak terminal rate pricing (seen at the September meeting) and February ’24.

- TD’s ECB call change, which looks for a 4.00% terminal rate, failed to impact pricing, with terminal still showing at/just below the 3.75% mark in deposit rate terms.

- Comments from ECB Vice President de Guindos are due later (at the IESE Banking Industry Meeting on the topic of “Banking Navigating the Wave of Inflation”), but that shouldn’t move the needle given his well-known stance (a little more dovish than the typical centre of the ECB), coupled with the fact that he has provided remarks in the recent past.

- A quick reminder that liquidity will thin out on Thursday, owing to the observance of the Ascension Day holiday across large chunks of Europe.

| ECB Meeting | €STR ECB-Dated OIS (%) | €STR ECB-Dated OIS At Previous Update (%) |

| Jun-23 | 3.374 | 3.375 |

| Jul-23 | 3.557 | 3.557 |

| Sep-23 | 3.647 | 3.638 |

| Oct-23 | 3.642 | 3.629 |

| Dec-23 | 3.591 | 3.569 |

| Feb-24 | 3.503 | 3.463 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok