Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

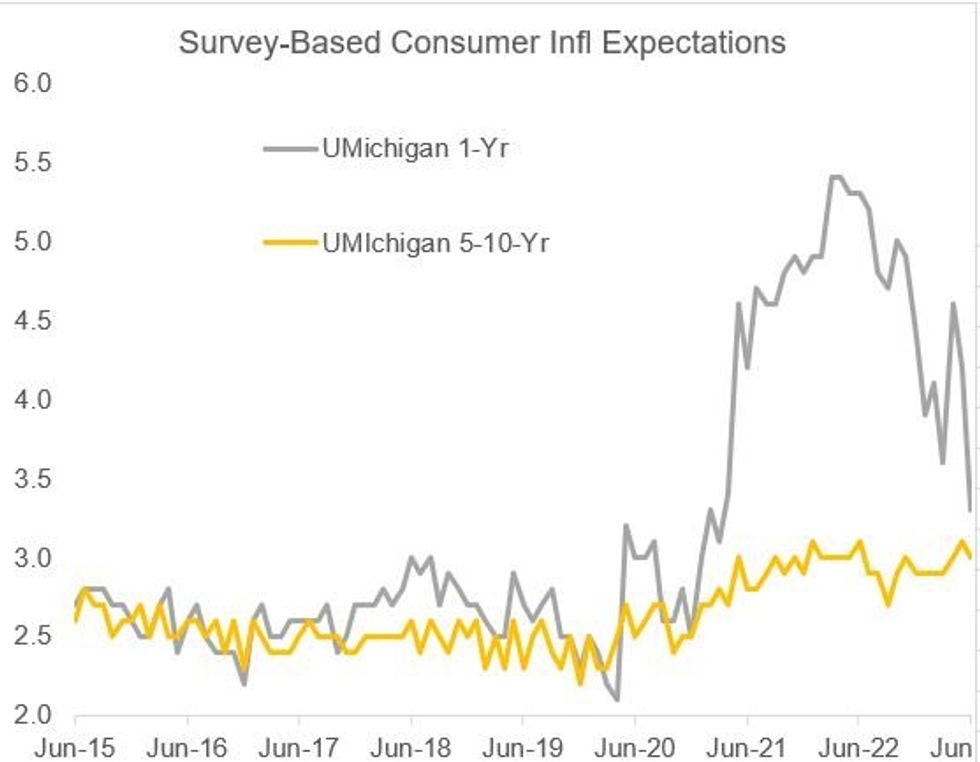

June's preliminary University of Michigan survey of consumers came in better than expected across the board: that included the overall sentiment figure of 63.9 (60.0 survey, 59.2 May), current conditions of 68.0 (65.1 survey, 64.9 May), and expectations of 61.3 (55.2 survey, 55.4 May).

- Most notably though, year-ahead inflation expectations came in way lower than expected at 3.3% (vs 4.1% survey, 4.2% May), with 5-10 year expectations dipping from May as anticipated at 3.0% (vs 3.0% survey, 3.1% May).

- The overall improvement reflected "greater optimism as inflation eased and policymakers resolved the debt ceiling crisis".

- While "sentiment remains low by historical standards as income expectations softened" and "a majority of consumers still expect difficult times in the economy over the next year", inflation expectations stole the show, with the 1-Y reading the lowest since April 2021.

- The report noted that despite concerns over higher interest rates, consumers saw affordability improve for durables, cars, and homes.

- All in all it was a report that suggested that with near-term - if not longer-run - inflation expectations pulling back, and activity cooling but remaining solid, the "soft landing" scenario that Fed Chair Powell discussed this week remains "possible", as he said.

- Much will depend on labor market conditions, which as noted in the UMichigan report seem to be deteriorating: "consumers overall shared concerns about a weakening labor market; they downgraded their own income expectations for the year ahead in both nominal and inflation-adjusted terms."

Source: UMichigan, BBG, MNI

Source: UMichigan, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok