Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

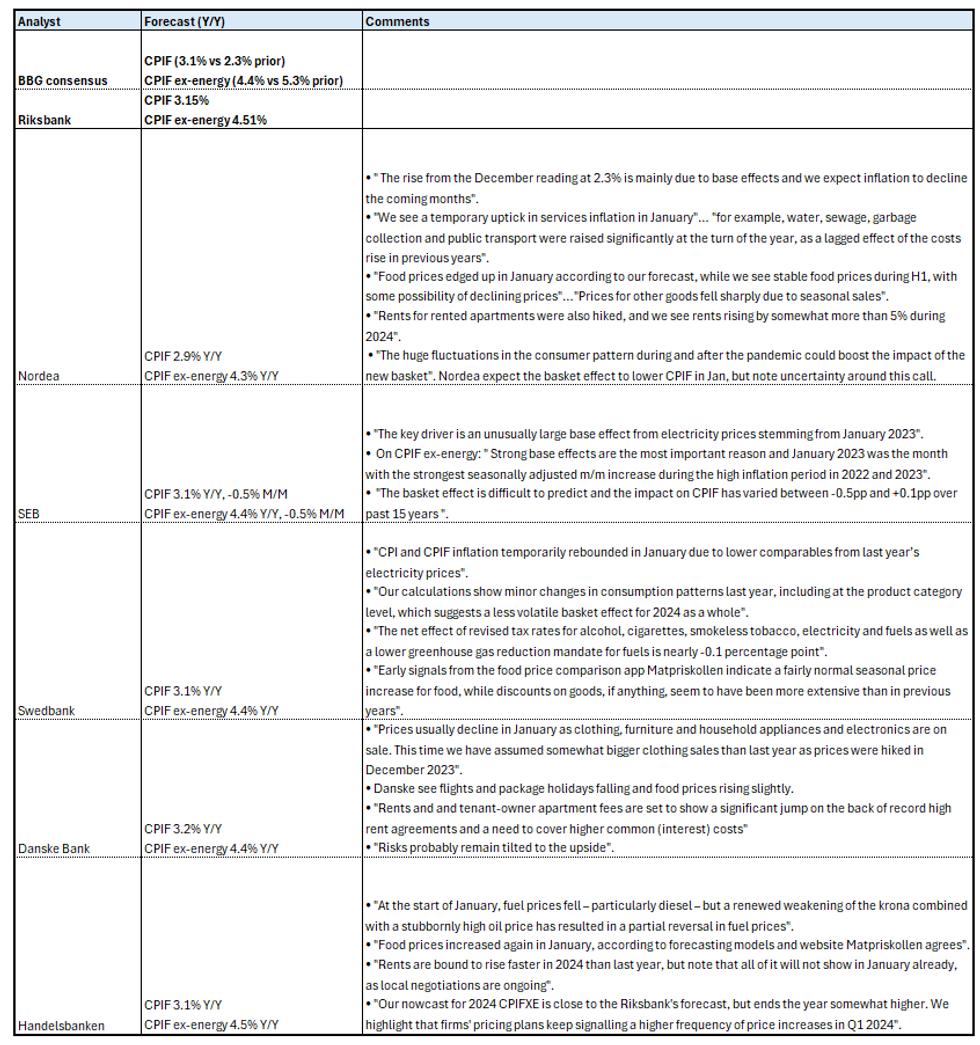

Sweden’s January CPI release is due on Monday at 0700GMT/0800CET.

- Analysts expect CPIF ex-energy to print at +4.4% Y/Y (vs +5.3% prior), with Nomura a standout on the downside looking for 3.9% Y/Y. The Riksbank's November MPR sees CPIF ex-energy at +4.51% Y/Y, although that forecast was made more than 2 months ago.

- Analysts note that the reweighting of the CPIF basket adds two-way uncertainty to the January print.

- Aside from this, electricity base effects are seen pushing headline inflation higher to +3.1% Y/Y (vs +2.3% prior; Riksbank exp. +3.15%).

- Services inflation may see a temporary uptick, with some analysts pointing to higher rents in January and expectations for that dynamic to play out across 2024 on the whole.

- Food prices are generally seen rising on the month.

- Markets will as always be sensitive to the inflation release, particularly after the Riksbank opened the door to rate cuts as early has H124 at its February decision.

- However, we suspect the bar to rate cuts is set quite high at this stage, and a run of downside inflation surprises will be needed before a March cut is even considered.

- We also believe the idea of a May cuts seems a little premature at this stage, but concede that there is plenty of data scheduled for release between now and then.

- Click for a selection of domestic analyst comments:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok