Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

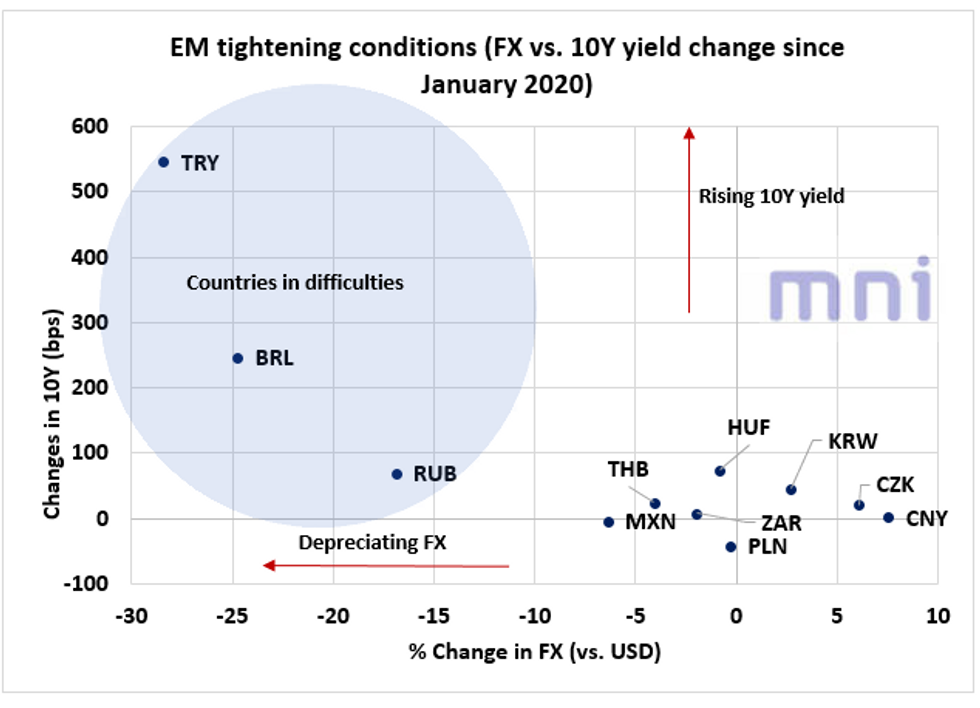

- We have seen that despite the USD weakness in the past year amid the sharp increase in the Fed's balance sheet assets to prevent the local (and global) economy from falling into a deflationary depression, three EM countries have remained under pressure in the past year: Turkey, Brazil and to a lesser extent Russia.

- The scatter plot below shows the changes in the 10Y yield (in bps) with the changes in the currency (in %, relative to the US Dollar) for most of the EM economies since the start of 2020.

- First, Turkey has been the most vulnerable place among the EM market amid rising political and economic uncertainty in addition to the increase in 'staff turnover' at the CBRT. TRY has depreciated over 28% against the USD and the 10Y yield has increased by nearly 550bps.

- The BRL has also been weak against the US Dollar amid rising political uncertainty and worsening Covid19 situation; the real is down nearly 25% against the USD since January 2020, and Brazil 10Y yield is up 245bps.

- While Russia 10Y has risen by 70bps (which is line with some of the other EM 10Y moves), the RUB has remained surprisingly weak despite the sharp recovery in oil prices (RUB is down 17% against the USD).

Source: Bloomberg/MNI

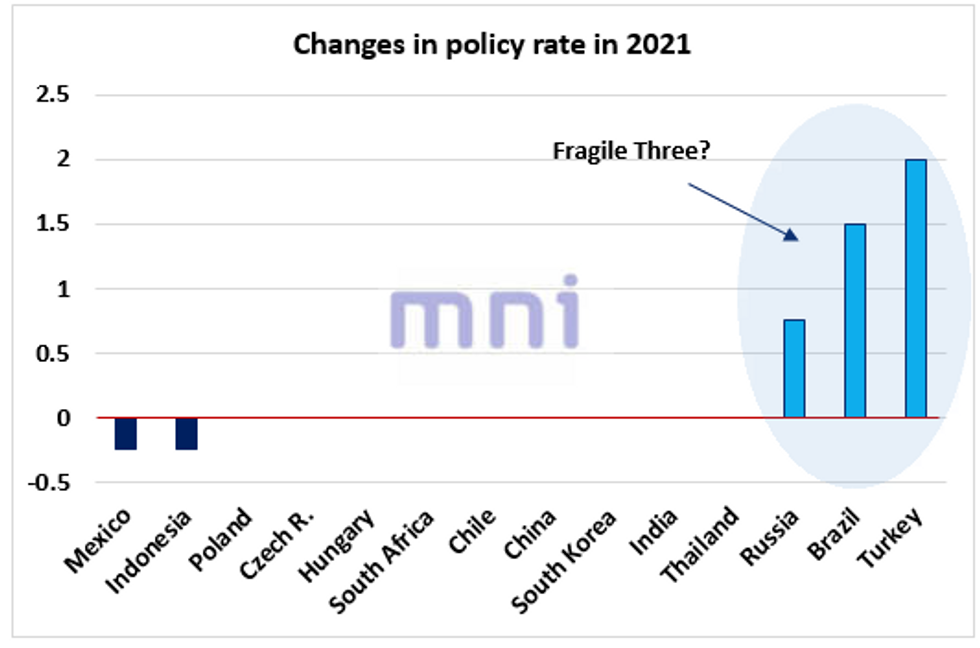

- As a result, the currency weakness in the 'Fragile Three' has pushed the CBRT, CBR and BCB to hike rates in 2021: Russia by 75bps, Brazil by 150bps and Turkey by 200bps, amid growing concerns over rising inflationary pressures.

- Yesterday, the BCB decided to raise its benchmark rate Selic by 75bps to 3.5% after CPI inflation rose to a four-year high of 6.1% in March, diverging significantly from the central bank's year-end goal of 3.75%.

- Hence, growth expectations for Russia, Turkey and Brazil could be reviewed to the downside as the significant tightening in financial conditions (in both short-end and long-end of the curve) could weigh on the economic recovery.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok