Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

DATA REACT

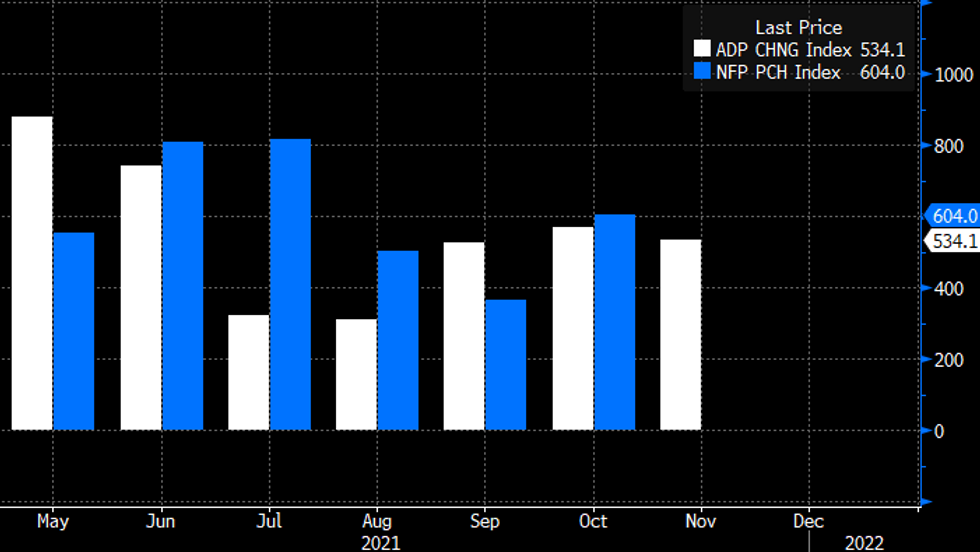

ADP jobs reports have been pretty consistent the last 3 months: nonfarm private employment estimated at +534k in Nov, vs +570k in Oct (only a 1k downward revision) and +526k in Sep (after a summer lull with +316k avg in Jul-Aug).

- For what it's worth, the October ADP was pretty close to the eventual BLS nonfarms private payrolls result (+604k).

- With Fed Chair Powell's comments yesterday implying the default position is for the FOMC to accelerate the taper at the December meeting, likely only a really weak nonfarm print this Friday (seen +525k private, +548 overall) would seriously put those plans into question (apart perhaps from Omicron developments).

- The Nov ADP reading certainly doesn't change the narrative.

- Of some note within the details: in the context of ADP jobs remaining 5mln short of pre-pandemic levels, professional services (+110k in Nov, behind only Leisure/Hospitality's +136k) joined construction jobs as moving above their Feb 2020 (ie pre-pandemic) level.

Source: BBG, BLS, ADP

Source: BBG, BLS, ADP

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok