Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNY

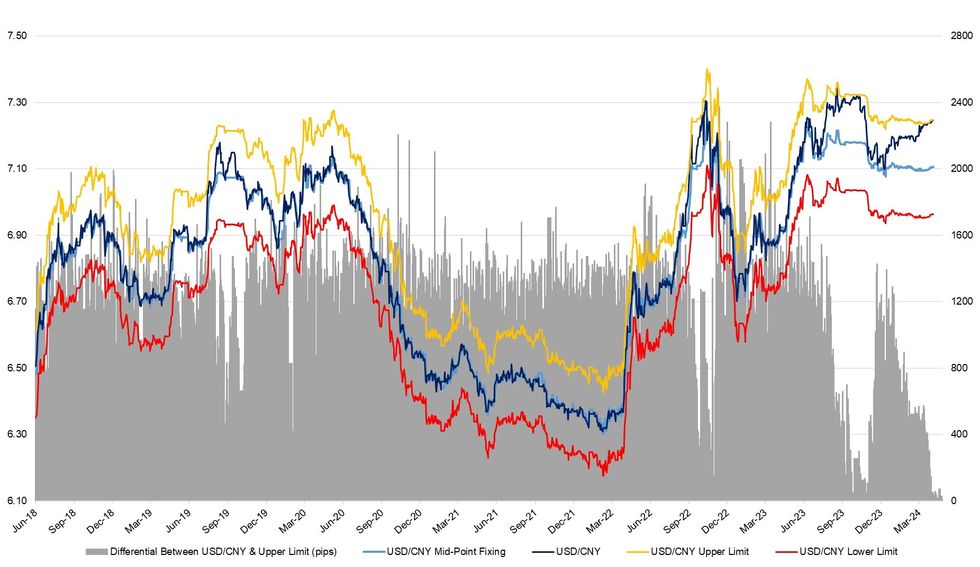

USD/CNY continues to trade in close proximity to the upper end of its permitted trading band (2% above the daily mid-point fixing).

- There has been some background talk of the potential for CNY devaluation given trends in Chinese metal holdings.

- To stress, that isn't a widely discussed matter, and remains a marginal risk at this stage.

- The PBoC has continued to lean against runaway yuan weakness via various channels in recent weeks.

- The most notable intervention came as the central bank deployed the largest bias for CNY strength on record vs. broader expectations earlier this month (measured via the actual fix level compared to the BBG fix estimate).

- Well-documented economic risks, a tepid economic recovery and broad expectations for further policy easing continue to weigh on the redback, while the broader USD bid also factors in.

- One factor to consider with potential CNY weakness is the relative export competitiveness if other major exporter currencies continue to weaken against the USD.

- CNY/JPY is already through it’s ’22 peak.

- CNY/KRW has faded away from ’24 highs after it failed to breach its ’23 peak.

- On that front, a policy advisor previously told our Beijing team that “the PBOC may consider increasing the yuan’s flexibility should it judge that CNY had been forced to appreciate against the basket currencies.”

- That is not a consensus view, with a trade advisor telling our Beijing team that China’s “forex policy should emphasise support for imports and stable financial markets over just boosting exports.”

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok