Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

The data calendar is busy for the coming week in China. We are still waiting for aggregate financing/new loans data for April. This could come out later today or over the weekend.

- Monday will bring the latest round of 1-yr MLF rate operations. Interestingly, the market consensus has shifted back to no change when it comes to the rate applied to using the facility. Earlier this week the consensus had been for a 5bp cut to 2.80% (from 2.85%). No doubt the firmer than expected inflation data, released earlier in the week, has played a role in shifting the consensus.

- April's monthly run of industrial production, retail sales and fixed asset investment data is also out on Monday. Not surprisingly, market expectations are fairly downbeat. IP is seen +0.5% YoY versus +5.0% previously, with retail sales seen -6.2% YoY (-3.5% YoY previously).

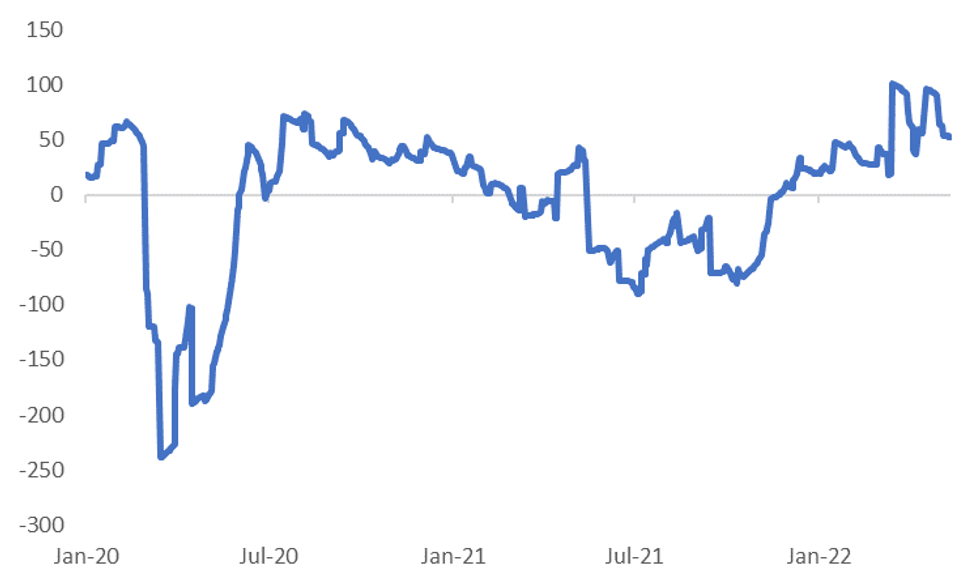

- China's economic surprise index has actually held up quite well in recent weeks, see the chart below. One possibility is that expectations have adjusted much quicker compared to the first Covid outbreak in early 2020, when the surprise index plummeted. Needless to say, if we do see downside surprises in Monday's data it could kick-off a fresh round of growth concerns.

- New homes prices print on Wednesday, then the 1yr and 5-yr LPR fixings are due on Friday.

Fig 1: Citi China Economic Surprise Index

Source: Citi/MNI- Market News/Bloomberg

Source: Citi/MNI- Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok