Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

China PMIs for May are the main data prints in focus for this week. The official PMIs print tomorrow, with manufacturing expected to print at 48.9, versus 47.4 in April. For non-manufacturing, the consensus is 45.0, versus 41.9 last month. For the Caixin manufacturing print (out Wednesday), the market expects a 48.8 outcome, from 46.0 previously.

- It is noteworthy the consensus estimate for the Caixin survey has come down. In the middle of last week, it was above 50.0, but we are comfortably below that level now.

- Last week we noted the PMI prints may have downside risks, relative to expectations of sequential improvement, as Standard Chartered's SME survey deteriorated further in May. This survey has a reasonable correlation with the manufacturing PMIs.

- Premier Li comments around 2022 being worse, in some respects, relative to 2020, also hit sentiment.

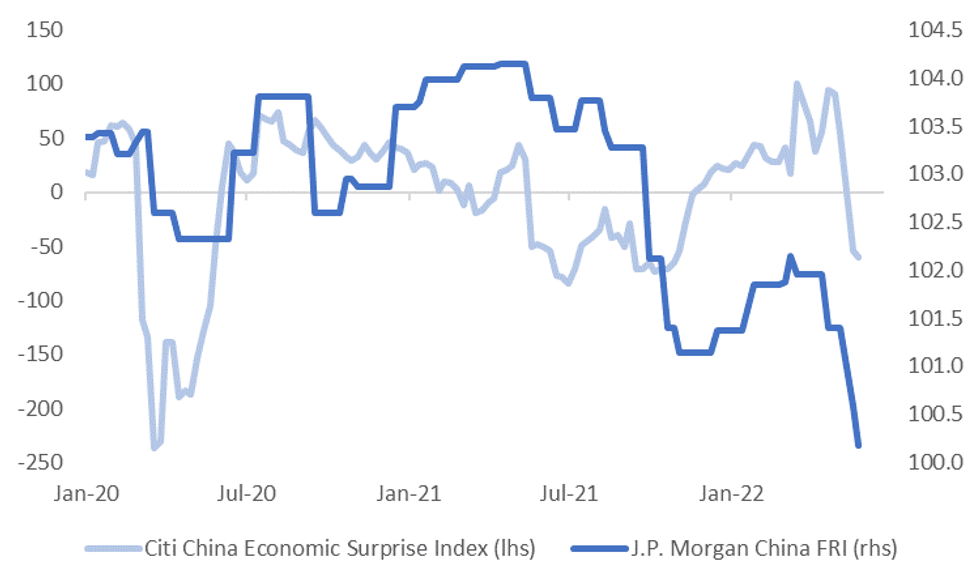

- Still, we have seen a meaningful adjustment lower in the Citi China economic surprise index, while the J.P. Morgan China growth forecast revision index (FRI) has also come down quite sharply, see the chart below.

- Hence the bar for further downgrades could be high. The market may also be encouraged by loosening Covid restrictions for Beijing and Shanghai and further stimulus measures, which potentially points to the worse of the growth headwinds being behind us.

Fig 1: Citi China EASI and J.P. Morgan China Forecast Revision Index

Source: Citi/J.P. Morgan/MNI- Market News/Bloomberg

Source: Citi/J.P. Morgan/MNI- Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok