Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

Next week's data calendar is light. Industrial profits print on Monday, but the official PMI prints for June on Thursday will have a stronger focus. The Caixin manufacturing PMI prints on Friday.

- Last month the manufacturing PMI rose to 49.6 from 47.4, while the non-manufacturing PMI got to 47.8 from 41.9.

- There are no consensus forecasts for any of next week's PMI prints yet. Arguably there have mixed drivers over the past month.

- The broader sense appears to be improved economic momentum in China, albeit still recovering from a low base. A divergence is likely to remain between the manufacturing and non-manufacturing sides, given on-going Covid testing and restrictions on consumer/services related activities.

- The external environment is also turning less supportive, given sharp falls in the EU and US PMI prints for June.

- Of course, if we see further sequential improvement in the China PMIs it may well further boost the China relative 'outperformance theme' that has been evident in equities and FX over the past month.

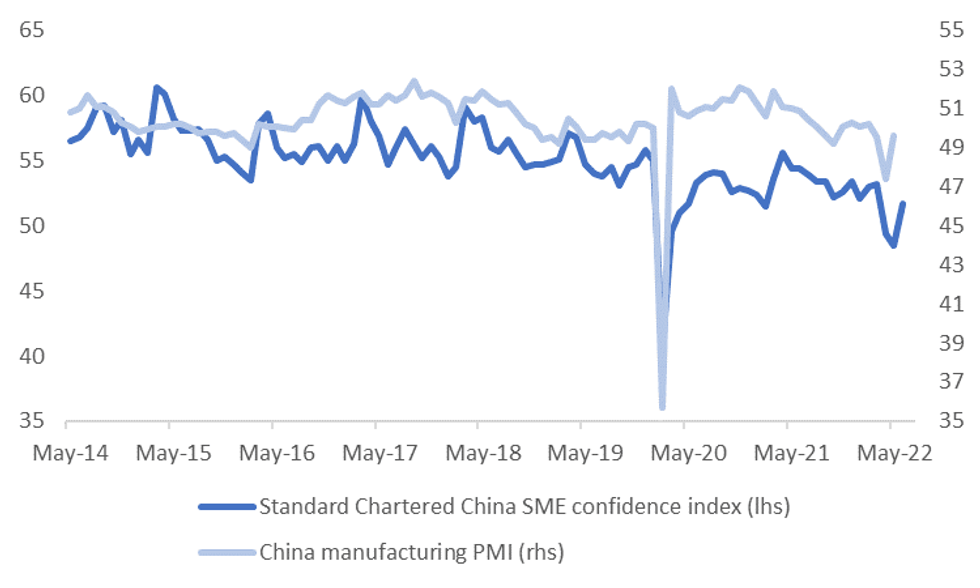

- Note, the Standard Chartered Bank survey of China SMEs has already printed for June. The confidence index rose to 51.7 versus 48.5 in May. The chart below plots this measure against the official manufacturing PMI. All of the components of the Standard Chartered survey improved.

- A caveat worth noting though is that last month the SC survey didn't point to improvement in the PMI prints.

Fig 1: Standard Chartered SME Survey & China Manufacturing PMI

Source: Standard Chartered/MNI - Market News/Bloomberg

Source: Standard Chartered/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok