Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

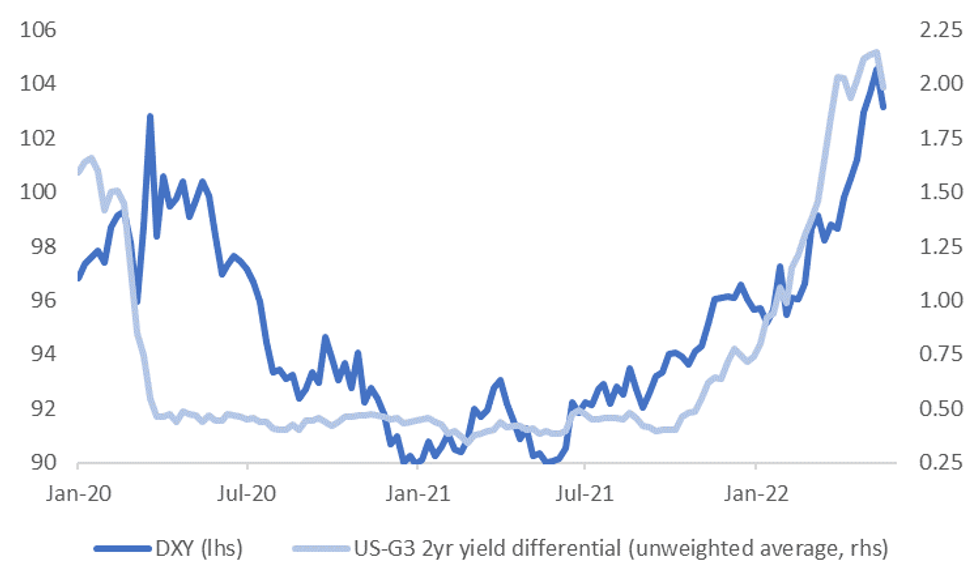

The USD is starting the week on the backfoot, the DXY is back sub 103.00, tracking towards last week's lows around 102.65/70.

- Last week saw a decent pull back in the yield differential for the USD against other core markets. The first chart below plots the DXY versus the unweighted 2yr yield differential with the G3 markets. The spread fell by 16bps last week, which is the largest weekly drop since the early 2020 period.

- US yields were relatively steady, with much of the waning yield differential reflecting higher EU and UK yields.

Fig 1: DXY & US Yield Differential

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- Still, stability in US yields no doubt helped. Fed expectations for end 2022/early 2023 have been fairly rangebound over this period.

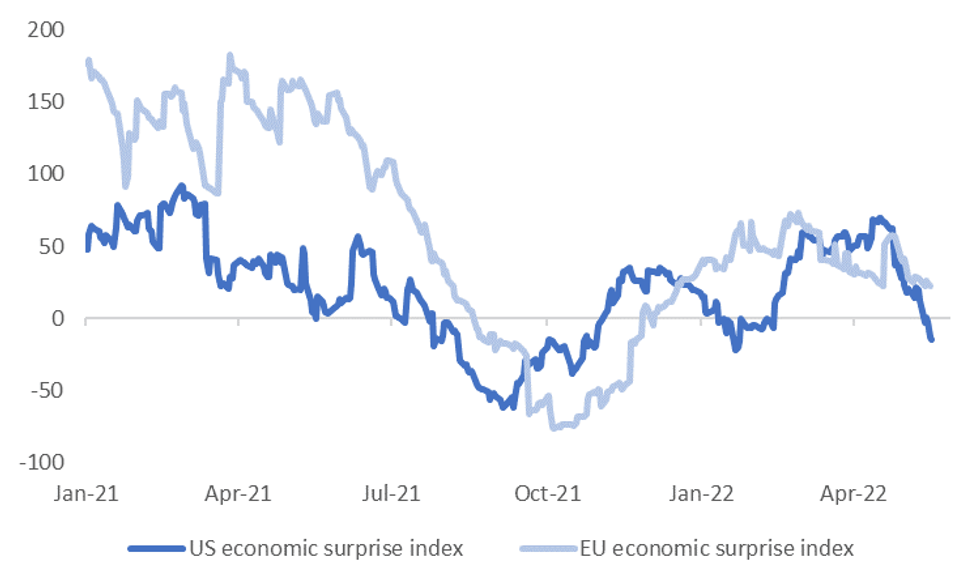

- As we highlighted last week, US data momentum has clearly rolled over, relative to expectations. The Citi US economic surprise index is almost back to year to date lows, see the second chart below. On a relative basis, there is now a reasonable wedge between this index and the equivalent reading for the EU.

- These relative shifts have weighed more on US growth expectations in recent weeks, at least according to the J.P. Morgan growth Forecast Revision Indices (FRIs).

- Better risk appetite, as reflected in higher US equity futures today, is also helping higher beta plays like AUD and NZD, although futures are off best levels. China and Hong Kong stocks are also struggling to replicate last week's strong performance in early trade today.

Fig 2: Citi US & EU Economic Surprise Indices

Source: Citi, MNI - Market News/Bloomberg

Source: Citi, MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok