Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

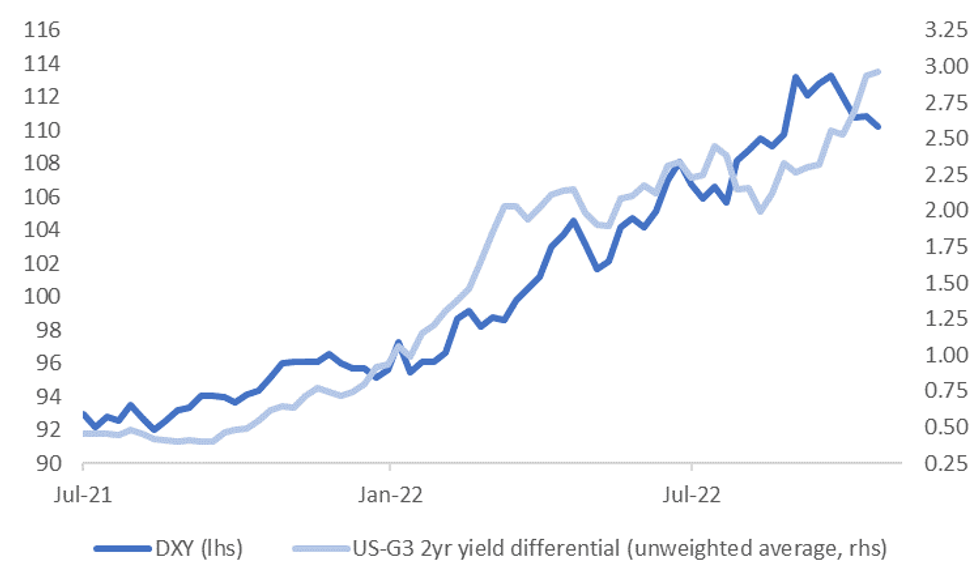

The USD is close to recent lows if the DXY and BBDXY indices are used as gauges. Both indices are below their respective 20 & 50-day EMAs. At face value this weakness is at odds with still decent yield premium over the G3 economies. The first chart below plots the DXY index against the unweighted yield differential between the US and G3 economies (for the 2yr tenor).

- The correlation between the two series has been high the past year, but is lower for the past 3 months (+20%).

- Currency markets may be positioning for a reduced pace of Fed tightening, although this is yet to show meaningfully in terms of yield differentials.

- There is also a sense that a Republican controlled Congress (if that's how results unfold) will be more fiscally conservative and therefore less inflationary, but again this be expected to be showing up more in relative yield differentials.

- Correlations between these USD indices and global equities is much stronger at the moment (in an inverse fashion), with the USD suffering as global equities rebound. Optimism around China shifting away from covid-zero is part of this rebound story, although the authorities are pushing back against a quick-reopening theme.

Fig 1: USD DXY Index Versus 2yr Yield Differentials

Source: MNI - Market News/Bloomberg

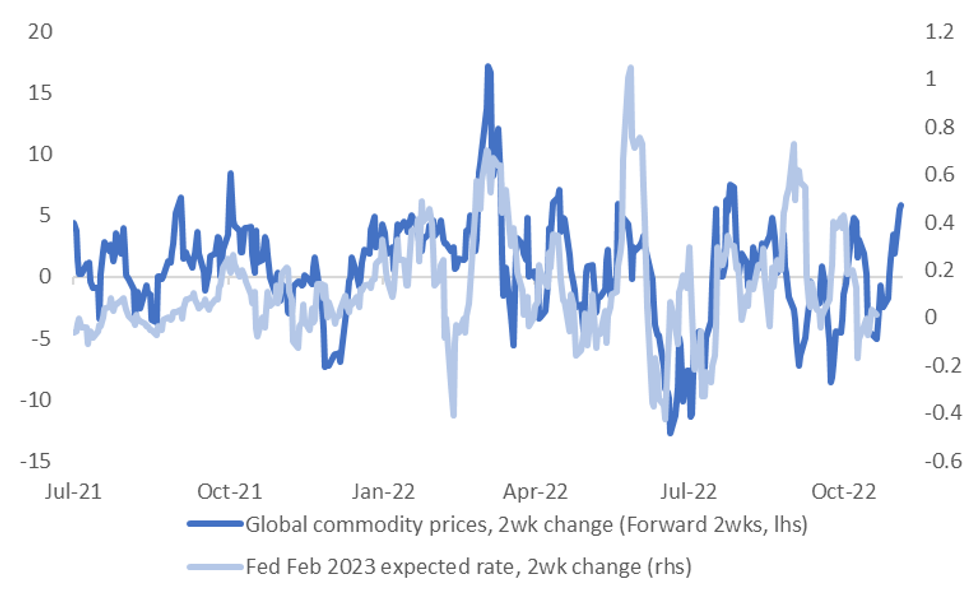

- Fed expectations for early next year are holding around recent highs. The recent rebound in commodity prices suggests some upside risks to pricing, although a lot is likely to depend on how the October inflation print unfolds later this week.

- In any case, further USD downside may need support from a weaker US yield backdrop at some stage.

Fig 2: Fed Expectations For Early 2023 & Global Spot Commodity Prices

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok