Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

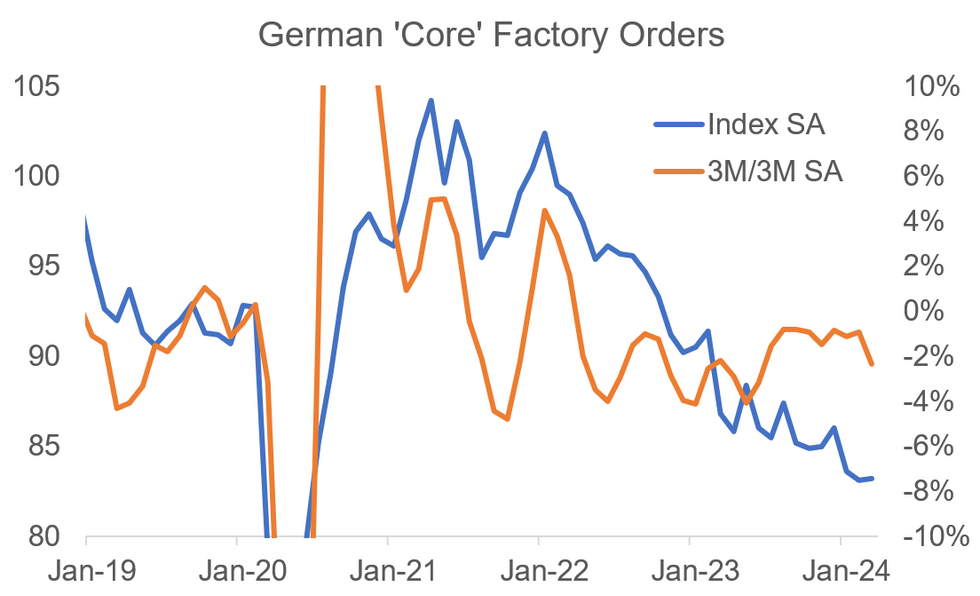

German factory orders fell by 0.4% M/M in March, softer than the +0.4% expected and an even bigger downside miss when considering a downward revision in February (by 1.0pp to -0.8% - all figures are real, SWDA). The underlying 'core' measure pointed towards some stabilisation, however.

- Factory orders fell 1.9% Y/Y (vs -0.7% consensus) vs -8.8% in February, with the improvement in the annual comparison mainly due to base effects.

- Core (ex-large ticket items) orders, a better measure of underlying activity, increased by 0.1% in March (vs -0.6% prior); its less volatile 3M/3M measure printed weaker than before, though, at -2.3% (vs -0.9% prior).

- The breakdown showed the slight 'core' rise was driven by foreign orders (+2.0% M/M vs -1.8% prior, the fastest growth in 4 months), with similar growth in both the Eurozone and non-EZ regions). In contrast, domestic orders decreased by 2.5% (vs +1.0% prior).

- From a category-by-category perspective, core orders rose in all main groups except intermediate goods, with durable goods a notable area of strength (+2.4% M/M vs +3.5% prior after a very weak Jan/Dec).

- Real manufacturing turnover meanwhile declined 0.7% M/M in March (1.1% prior, downwardly revised 1.1pp), adding to evidence that data released Wednesday will show industrial production ended its recent 2-month in March (-0.7% cons vs +2.1% prior).

- Overall, even though core orders are stabilising, the data looks weak compared with other recent German economic prints and soft domestic orders continue to point to an export-led rather than domestic-demand fuelled recovery. Looking ahead, while the key surveys (PMI and IFO) both suggested that manufacturing activity improved in April, they also both remained in contractionary territory.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok