Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

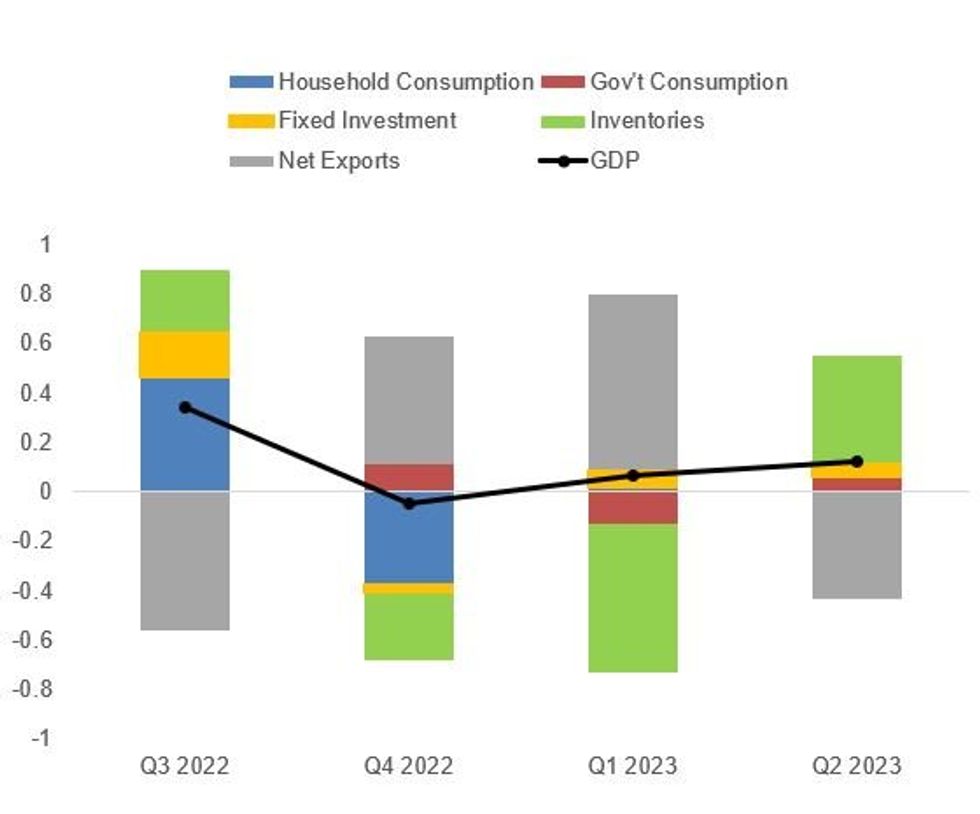

The unexpected downward revision to Q2 Eurozone GDP (+0.1% Q/Q vs 0.3% in the first reading) has spurred some negative reassessments of the EZ growth trajectory going into next week's ECB decision (and updated staff projections which penciled in 0.3% for the quarter).

- Yesterday's final Q2 GDP release showed weak private domestic demand (private consumption flat for 2nd consecutive quarter, fixed investment +0.3% Q/Q same as the prior quarter), a negative contribution from net exports (-0.4pp vs +0.7pp in Q1, due to a contraction of exports vs higher imports).

- A +0.2% Q/Q performance in gov't consumption (-0.6% prior), and a +0.43pp contribution to GDP from inventory buildup, helped underpin the quarter's growth reading.

- Effectively Eurozone output has stagnated since Q3 2022, growing just 0.17% total in real terms over the last 3 quarters, with domestic demand down 0.7%.

- While we've seen some positive comments regarding the weakening of the eurozone labour market, the overarching factor is that productivity remains moribund. Employment grew 0.2% in Q2 (0.5% in Q1, 0.3% in Q4 '22), with hours worked likewise up 0.2% (0.9% in Q1, 0.2% in Q4 '22).

- In turn the ECB's calculation of Unit Labor Costs hit the highest since Q2 2020 at 6.5% (vs 6.0% prior and 4.7% in Q4 '22). While that is calculated per capita rather than per hour (which Eurostat will release in next week's quarterly Labour Force Survey), there's little doubt that stagflation is a reasonable description of the current state of affairs.

Percentage Point Contributions To Q/Q Eurozone GDPSource: Eurostat, MNI

Percentage Point Contributions To Q/Q Eurozone GDPSource: Eurostat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok