Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

The first 20-days trade data for December was not as bad as likely feared. Exports were down -8.8% y/y, versus -16.7% for the first 20-days of November (note full month export growth for November was -14.0% y/y). There was no difference for daily average exports, -8.8%. Chip exports were still weak at -24.3% y/y.

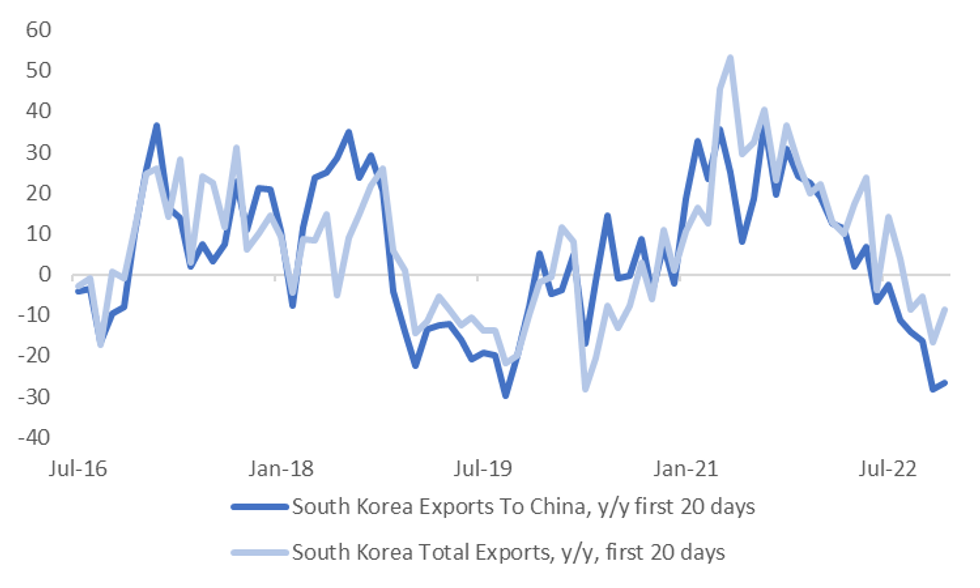

- Exports to China remained weak, down -26.6% y/y, although this was slightly better than the prior month (-28.3%). Exports to the US though recovered further, up 16.1% y/y, versus +11% in November.

- This has helped the overall export trend look a little better relative to exports to China, see the chart below.

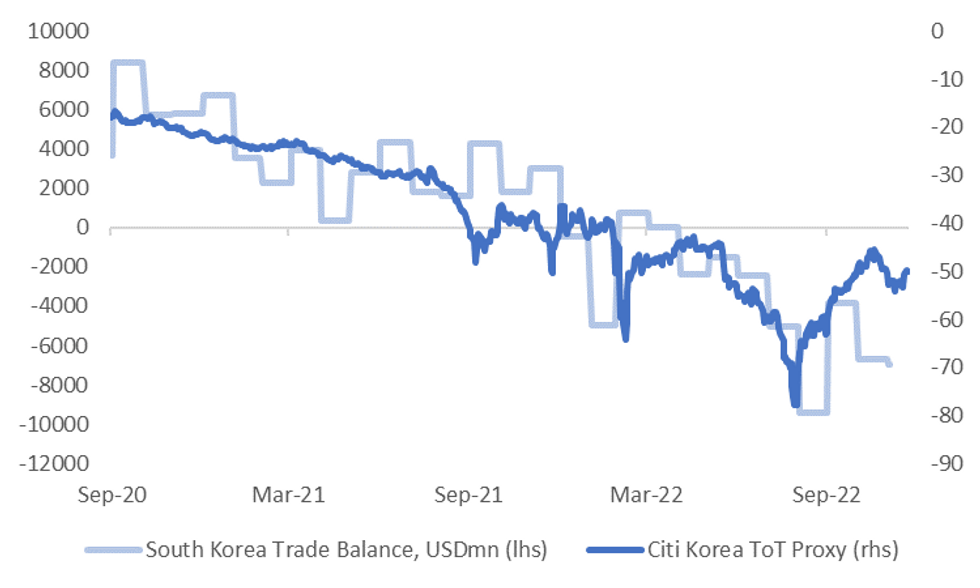

- Imports rose +1.9%, versus -5.5% last month. This kept the trade deficit wide at -$6.43bn. The trade position still appears to be lagging the improvement seen in the Citi terms of trade proxy since late August.

- So, we may see further improvement in the underlying trade balance position as we progress through the early stages of Q123, see the second chart below.

Fig 1: South Korea Export Trend Shows Modest Improvement

Source: MNI - Market News/Bloomberg

Fig 2: South Korea Trade Balance & Citi ToT Proxy

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok