Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

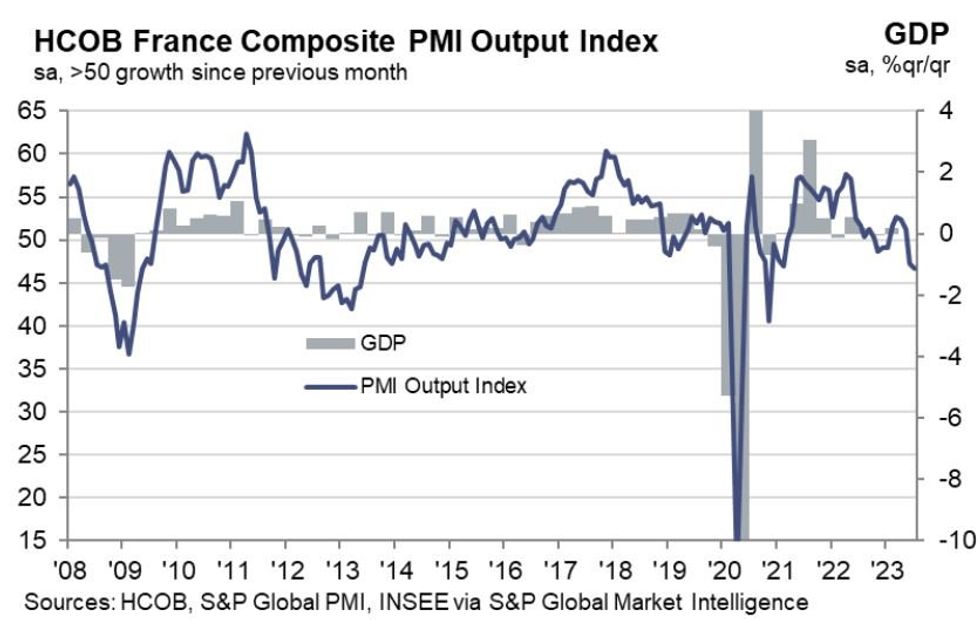

French July flash PMI Manufacturing came in at at 38-month low 44.5 vs 46.0 expected (and 46.0 prior), with Services at a 29-month low 47.4 vs 48.5 expected (48.0 prior), dropping Composite to 46.6 vs 48.0 prior.

- This was the worst Composite outturn since Nov 2020 and suggested that the suggested contraction in French activity at the end of Q2 was deepening going into Q3 (see chart).

- As more broadly in Europe in this round of PMIs, this was largely a weaker demand story: new business fell for a 3rd consecutive month and at the fastest rate in over 2.5 years, with backlog-clearing helping prop up activity.

- Notably export business dropped sharply, with the report noting softer Chinese demand than had been hoped.

- That meant French input/output costs falling to the lowest in over 2 years, though there appeared to be some divergence here, with manufacturers reporting lower raw material prices and service providers noting higher wage bills.

- A couple of positive areas: job growth continued (albeit at the weakest rate of 2023), while confidence strengthened vs June again led by Services firms (manufacturing sentiment remained pessimistic).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok