Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

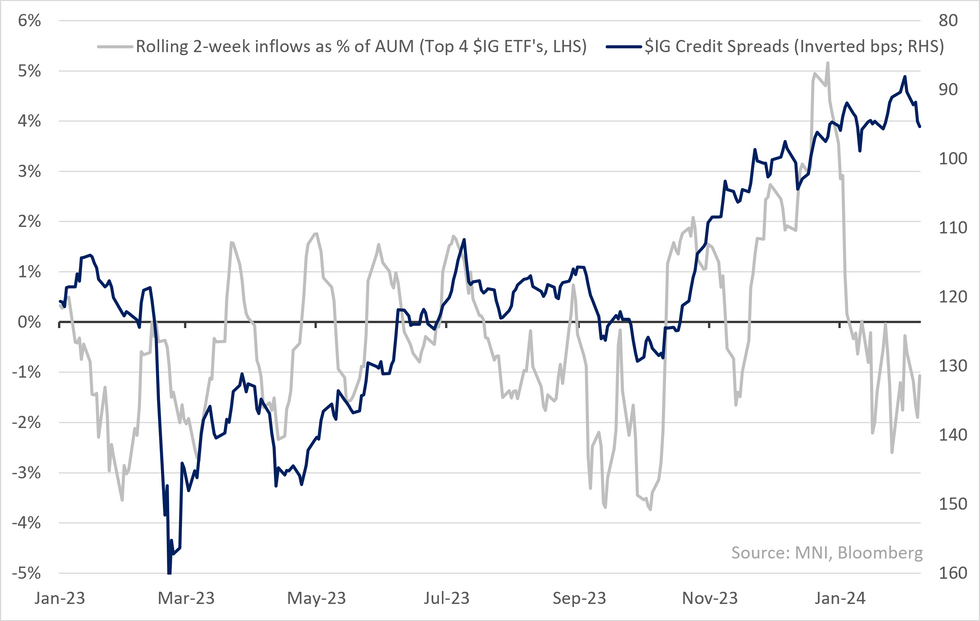

* To the week ending Wednesday there was broad easing in credit flows; $HY, €IG & £IG all reversed to outflows while €HY saw more muted inflows. only sector to see more inflows was $IG.

* $IG spreads failed to find support from the strongest weekly inflows in 4 weeks - it's underperformed local spreads WTD (+5.1 vs. +2.7) & in a broad based sell-off (corps & fins moved ~in-line and on-par move across spread-curve). Equities equivalents & rates that are unch through the week leaves above consensus $IG supply ($53.1 vs. c$35b) as the likely driver. The lack of support for flows doesn't bode well heading into March.

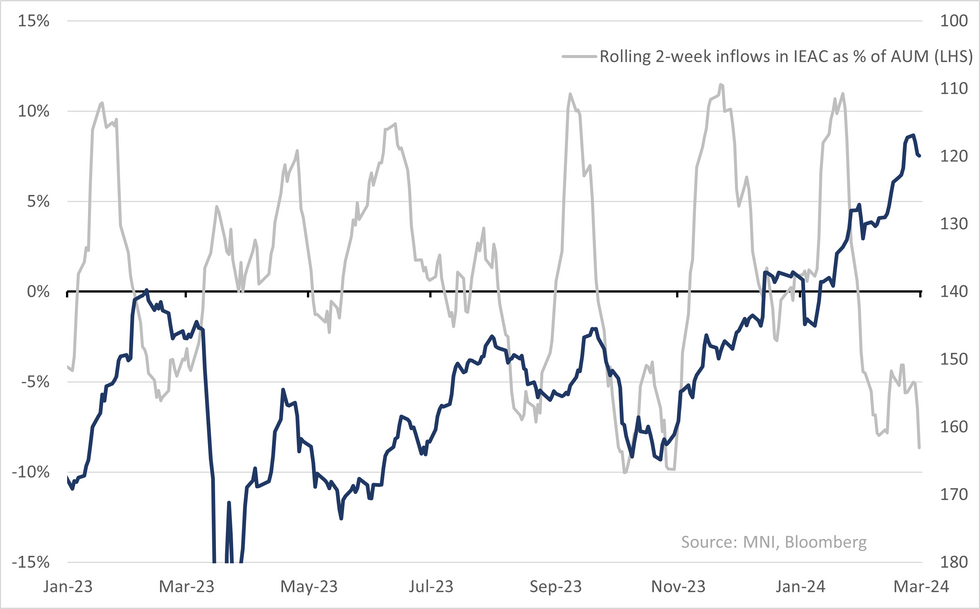

* ETF data since Wednesday point to a continuation of above; ~$500m of outflows from $HY ETF {HYG US Equity} yesterday while $IG inflows remain flat. Local €IG ETF {IEAC LN Equity} continues to see weakness - rolling weekly outflows are at -$1b.

* Outside of credit; streak of Chinese equity inflows finally ended but there was ongoing strong inflows into US equities driving net strong inflows. Govvies across US/Euro continued to see inflows.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.