Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HEALTHCARE

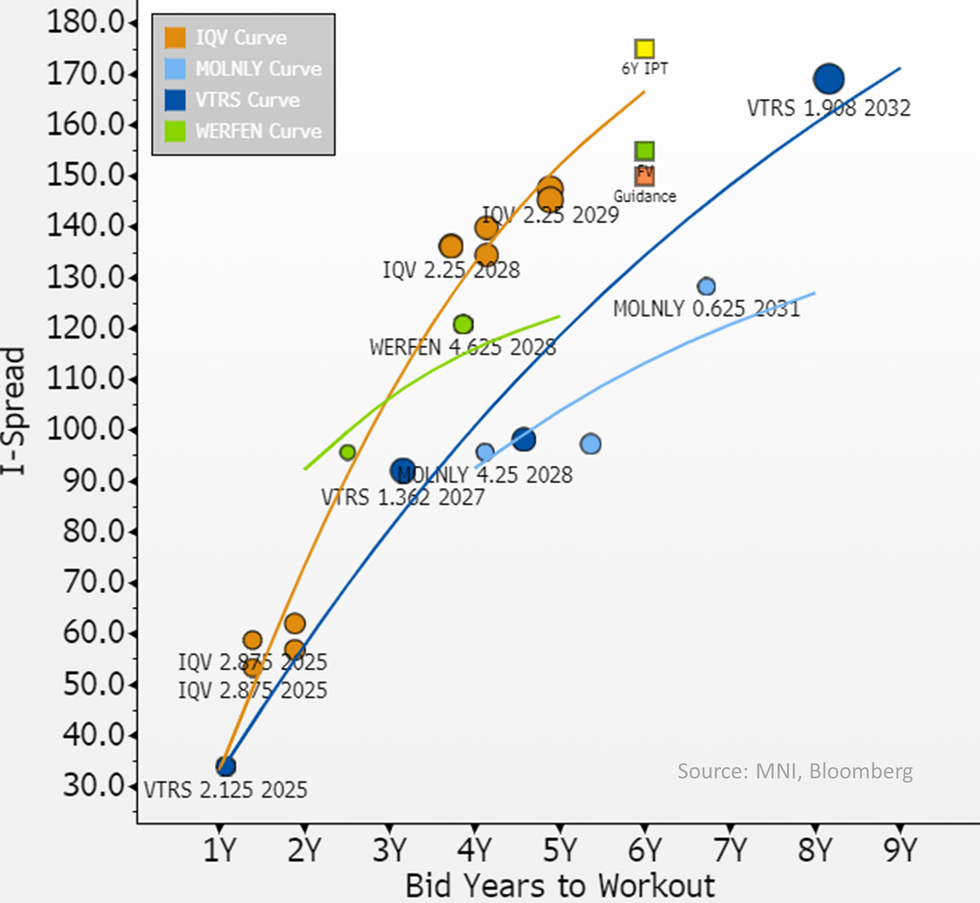

€500m 6Y IPT was +175, Guidance is +150 (books>€1.9b) vs. our FV +155 - secondary including 28s screened wide (we were typing when guidance came out) so guidance coming through our FV looks like a repricing on the name.

FV's are always based on existing secondary & 28s at +120 do trade - it screens more attractive here than the new issue at ~150.

- Relevant diagnostic comp's like Danaher & Thermo Fisher are higher rated & others like Bio-Rad & Quest Diagnostics only issue in $ - we've added back in pharma Viatris for that reason.

- We expect pricing inside larger scale health tech/research services name Iqvia (Ba2, BB; S) - 28's have rarely moved outside it. We do expect pricing outside heavyweight pharma VTRS which we have no issue with (we have a screen cheap view on the VTRS27s).

- Separate to pricing, Werfen does trade wide for ratings. Granted this is a private co but so is equal rated Swedish medical device co Molnlycke that trades 30bps inside on the 28s - granted much larger in scale (x10) but is single rated & seems to have elevated vol on earnings.

- 28s may screen cheaper than new issue (front bond maturity). Fair warning Werfen 28s are still at relative tights to it - I.e. flows may not enable compression to FV.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok