Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FISCAL

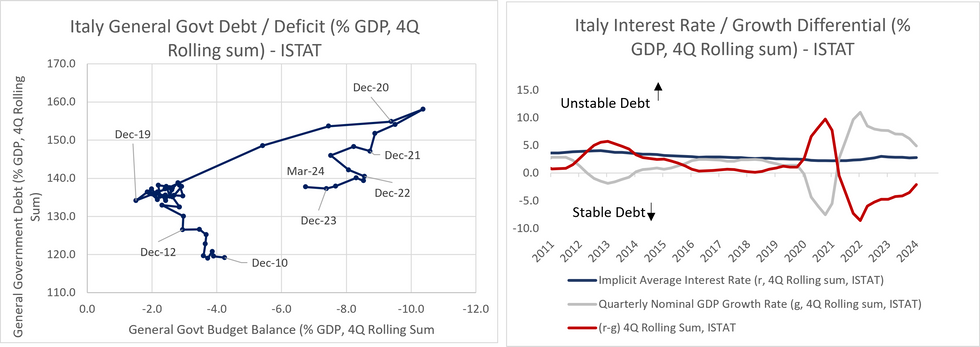

Recent trends in the interest rate-growth differential “(r-g)” remain somewhat concerning. The sharp fall in Q1 nominal GDP growth (-6.6% Q/Q) meant that the 4Q rolling sum of (r-g) rose to -2.1pp, its highest since June 2021.

- If (r-g) is positive and a country runs fiscal deficits, it puts the government debt/GDP ratio on a potentially unstable and explosive path higher.

- The Italian debt/GDP ratio rose a touch to 137.7% in Q1 (vs 137.3% prior), and the EC expects this ratio to rise to 141.7% by 2025.

- The EC notes that this increase “mainly reflects a less favourable interest growth-rate differential and a debt-increasing stock-flow adjustment related to the delayed cash impact of government-supported housing renovation”. The latter point refers to the controversial “Superbonus” scheme.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok