Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

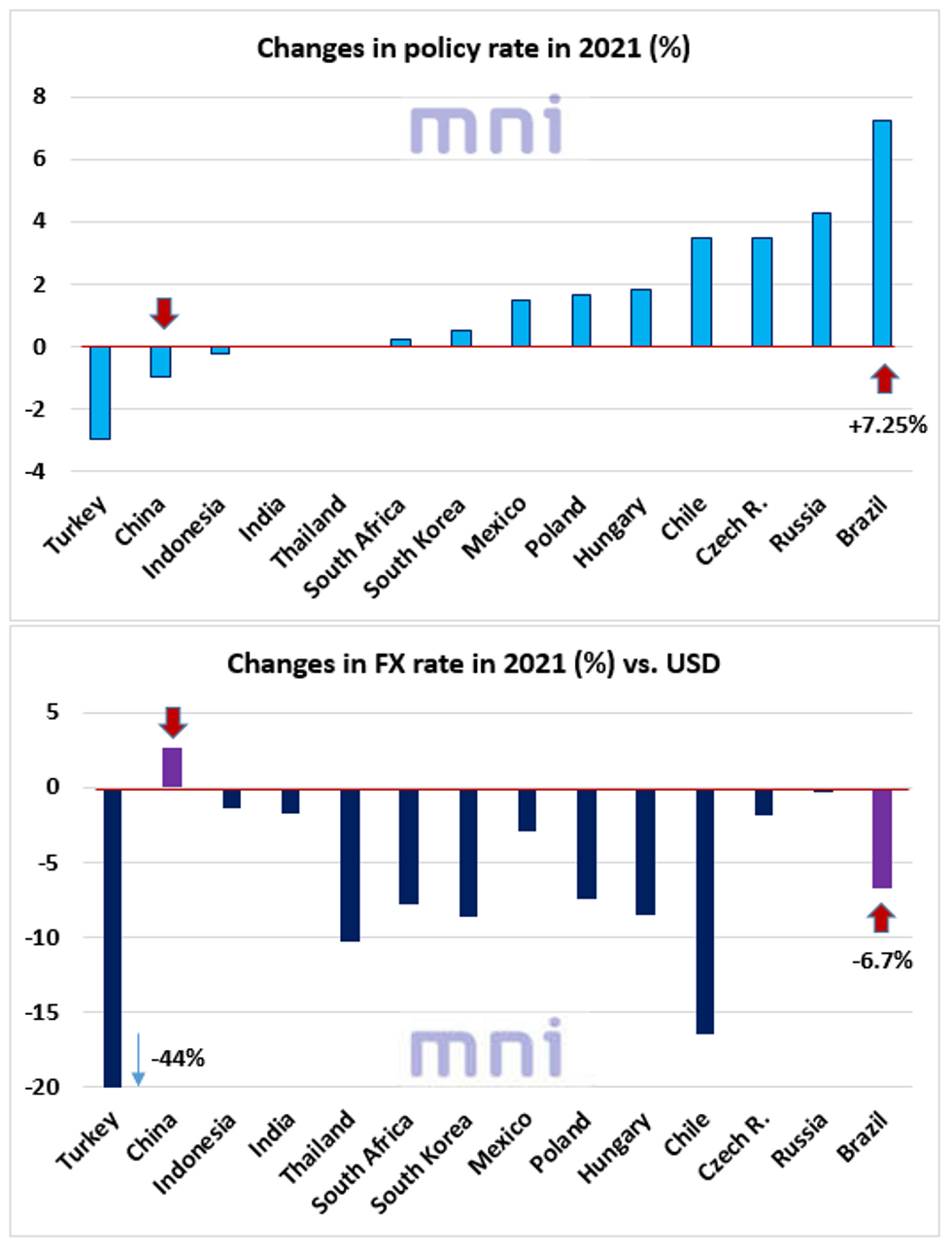

- Last year, the significant rise in inflationary pressures have resulted in aggressive hikes by EM central banks (CEEMEA/ Latam).

- Policymakers have not hesitated to surprise market participants by raising the policy rates more than expected proceed with up to 200bps hikes.

- Most of the effort done by EM policymakers was to limit the downside risk in the domestic currency as a depreciating currency keeps supporting inflation expectations.

- Interestingly, the chart below shows that to the exception of the Chinese Yuan, all the major EM currencies were down against the US Dollar in 2021.

- TRY has been the worst performer as the dovish CBRT and the political instability have been significantly weighing on the Lira (TRY is down 44% against USD in 2021).

- Interestingly, BRL is also down ‘significantly’ considering the aggressive tightening cycle run by the CBB; Brazil run the most aggressive tightening cycle in 2021, raising the Selic rate by 7.25% to 9.25% last year, but the BRL was still down 6.7% against the USD.

- This shows how strong the selling pressure was on EM currencies in 2021; what would have happened to the BRL if the CBB run a looser policy last year, or, even worse, joined the CBRT trend and cut interest rates to ‘stimulate’ the economic activity?

- Investors now curious to see if the 2021 effort will payoff this year with EM currencies consolidating significantly higher despite Fed preparing for hiking.

- Political uncertainty may still continue to weigh on some EM currencies (i.e. RUB, PLN, HUF) in the medium term and preference for ‘safe’ assets such as the USD may also remain strong if China growth continues to disappoint and momentum on the greenback resumes later on this year.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok