Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

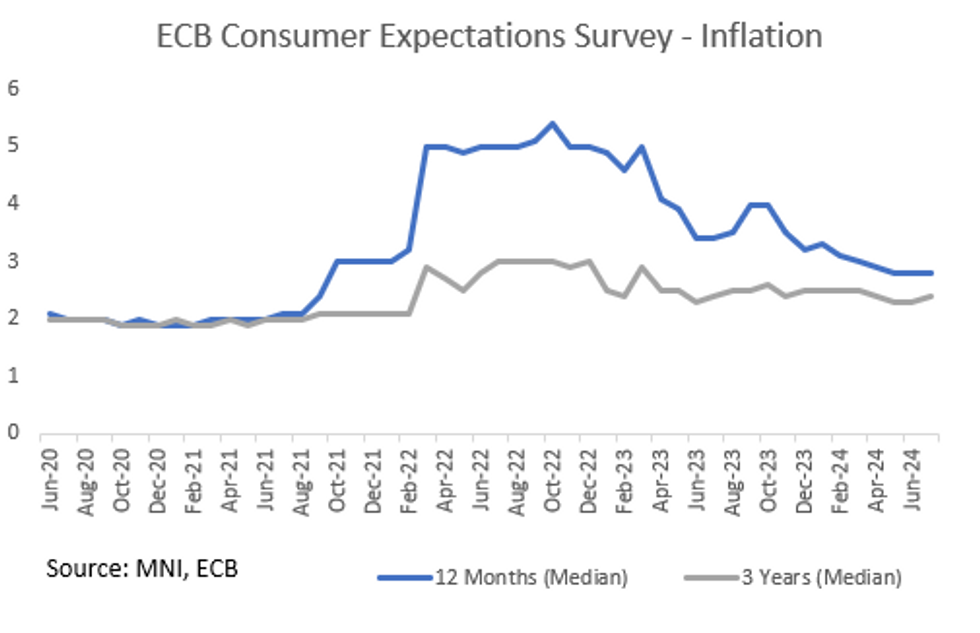

Eurozone consumer inflation median expectations on both the 1 and 3-year ahead horizon came a touch above expectations; the 1-year ahead print remained at 2.8% Y/Y for the third consecutive month (vs 2.7% consensus - but only from 3 analyst estimates), whilst the 3-years ahead increased to 2.4% Y/Y (vs 2.3% consensus from 5 analyst estimates and prior), as measured by the ECB's CES survey.

- The 1-year ahead median inflation expectation therefore remained at the lowest level since September 2021, whilst the 3-year measure returned to March's level.

- Meanwhile, consumer nominal income growth mean expectations for the year ahead decreased to 1.1% from 1.4% in June- the lowest since October 2023.

- Finally, and of note, the mean expectation for economic growth over year ahead weakened further to -1.0% from -0.9% in June - although still remains higher than March's -1.1% reading. This deterioration is not surprising, following ECB's Lagarde citing downside risks to growth in the July press conference and recent growth-related data consistently printing below expectations in recent months (this is displayed by Citi's economic surprise index which has been falling consistently in the last few months).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok