Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

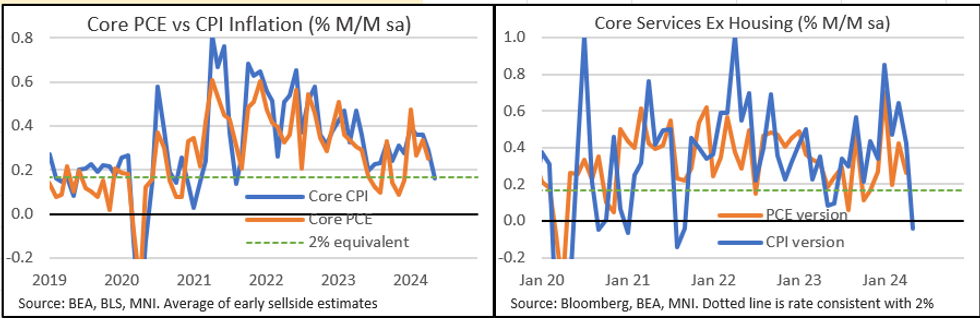

Just to note for the Fed's preferred inflation gauge of PCE, which for May is due out at the end of this month (Jun 28):

- As we noted earlier, the supercore (services-ex housing) CPI drop was driven in large part by auto insurance and airfares. However, PCE uses different measures for each of these categories, from the PPI report (which is out Thursday morning).

- PCE has been running cooler than CPI for a while now, in part because a) its auto insurance measure has been softer than CPI's due to methodological differences and a lower weighting and b) CPI's higher weighting for housing vs PCE.

- In this regard, it's possible that the spread of PCE and CPI looks a lot smaller this month, if the the equivalent PPI categories for airfares/auto insurance, and other categories that go from PPI>PCE (portfolio management, healthcare services), look more typical.

- Core PCE came in at 0.249% M/M in April. Pre-CPI release expectations for core PCE included Goldman Sachs’ 0.19% M/M (vs their forecast of 0.25% core CPI) and Nomura’s 0.234% (vs 0.31% core CPI). We're awaiting updated estimates.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok