Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

IDR

USD/IDR opened weakened but has pushed back towards the 14960 level, close to highs form late last week. The 1 month USD/IDR NDF got above 15000 post the Asia close on Friday, but we are now back to 14974.

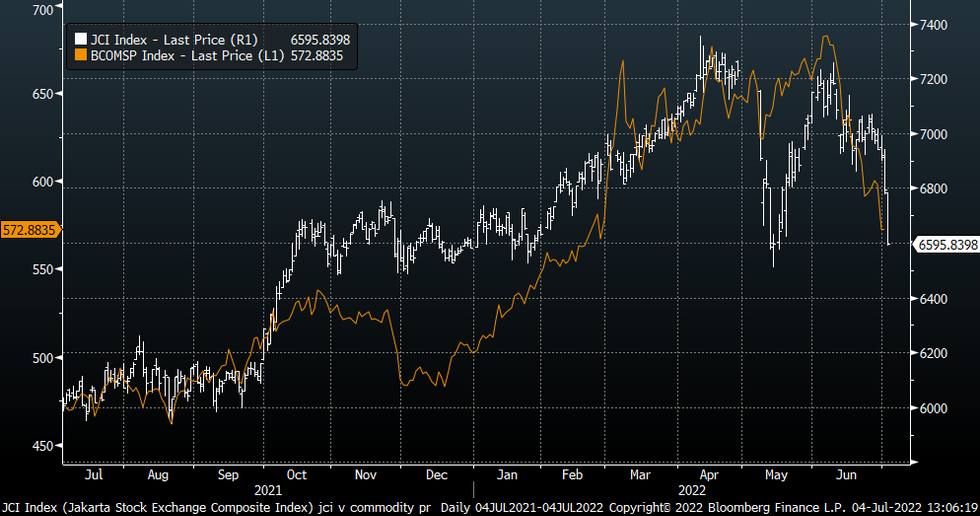

- Indonesian equities are down sharply today. The JCI is off by over 3%, marking the 6th straight session of declines. This looks to be some catch up with lower global commodity prices, see the chart below.

- Offshore investors were net sellers of Indonesian equities in June (-$501.3mn). This reverses the trend from earlier in the year when net inflow momentum was quite strong.

- Coupled with on-going liquidation of foreign holdings of local bonds paints a bearish portfolio picture.

- This has offset some of the positives for the currency in terms of lower core yields through last week.

- Locally, Indonesia has raised it export quota for palm oil, with producers now able to export at a rate of 7x their domestic sales, up from 5x. This is aimed at reducing domestic inventory levels.

- On the data front, the Danareksa consumer confidence number is due in the first half of this week. Foreign reserves are out on Thursday, while the BI consumer confidence number prints on Friday.

- BI continues to push back against rate hike expectations, stating rates will not pushed higher until core inflation pressures are more evident. Last Friday, core printed at 2.63% versus 2.70% expected for June. Headline moved above the BI target band (2%-4%) to 4.35% YoY.

Fig 1: JCI Versus Global Commodity Prices

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok