Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

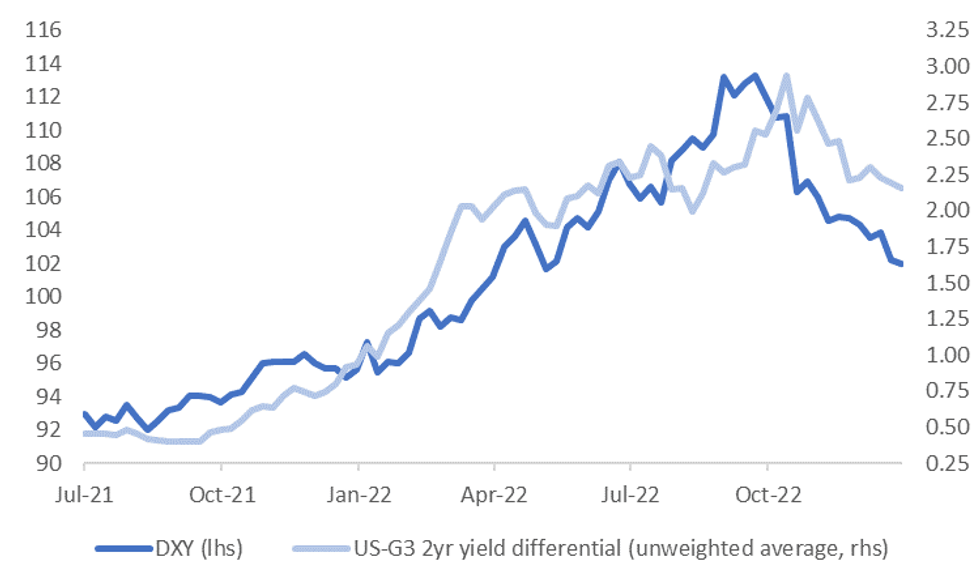

The USD is starting the week off on the back foot. The BBDXY remains off by 0.20% at this stage, around the 1222.40 level, the DXY is off by slightly more, -0.30%, due to the higher EUR weigh in the index. Broadly the USD continues follow yield momentum lower. The first chart below plots the DXY against the unweighted 2yr government bond yield differential with the G3.

- Visually, the DXY looks to have moved too much off its 2022 peak relative to yield trends, although trends in the series continue to match up with each other reasonably closely.

- The most notably compression has been in US-EU spreads, which have fallen by nearly 100bps in the 2yr government bond yield space since the USD peaked. For Japan, moves have obviously been more evident at the back end.

- The other positive for the EUR has been the continued recovery in the terms of trade proxy. Both this factor and yield momentum still point to higher EUR levels from here.

Fig 1: DXY & US-G3 Yield Differential

Source: MNI - Market News/Bloomberg

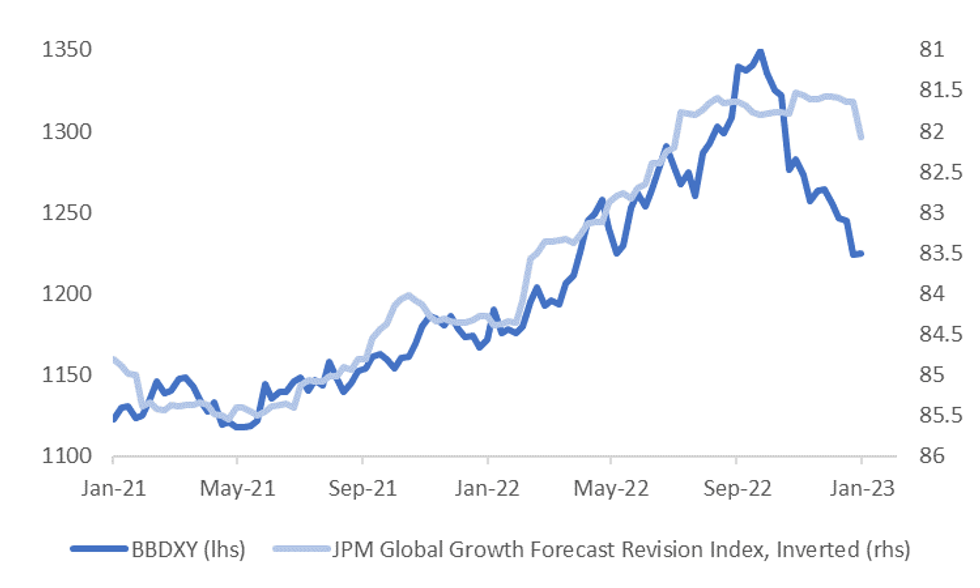

- The other factor to be mindful of is the improvement in global growth sentiment. Last week the J.P. Morgan Global Growth Forecast Revision Index (FRI) rose noticeably. The second chart below plots this index (inverted on the chart) against the BBDXY index.

- Downward revisions to global growth expectations were a USD positive through 2021 and 2022.

- Whilst US growth expectations were nudged higher last week, so too were China and EU prospects. Indeed, the consensus for China growth this year sits at 5.0%, up from 4.8%.

- China markets are closed this week, however, we will get fresh updates on the global outlook in terms of preliminary PMIs for January for the EU and the US.

Fig 2: J.P. Global Growth FRI (Inverted) & BBDXY

Source: J.P. Morgan, MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok