Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

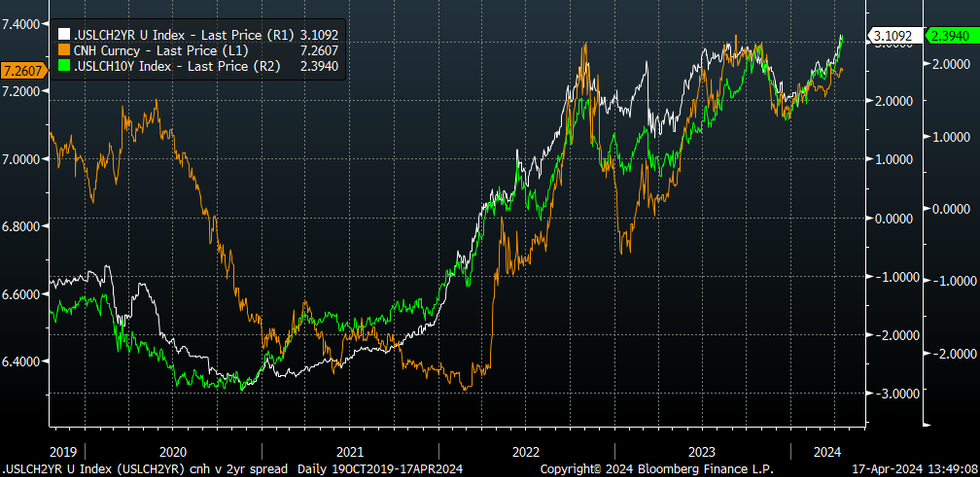

USD/CNH is slightly lower, last near 7.2600, but has maintained tight ranges overall in the first part of Wednesday dealings. This keeps us comfortably within April to date ranges.

- Sources of support have been from the steady CNY fixing outcome. Yesterday's set above 7.1000 saw USD demand emerge, but there was no follow through. The authorities are still guarding against the pace of depreciation.

- CNH liquidity also remains tight. The 1 month CNH Hibor in HK above 5%, close to fresh highs since 2018. Still, US-CH government bond yield differentials point to higher USD/CNH levels see the chart below.

- Insofar as these differentials represent a rough proxy for monetary policy differentials between the two economies, it suggests downside in USD/CNH will be limited in the near term, albeit without a sharp pull back in spreads.

- Some sell-side analysts have turned more cautious on further China policy easing post yesterday's Q1 GDP beat, but tightening is clearly not on the agenda.

- Onshore USD/CNY spot is also showing very limited downside and continues to trade close to the top end of the daily fixing band, which still suggests underlying onshore depreciation pressures.

Fig 1: USD/CNH Versus US-CH Government Bond Yield Differentials

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok