Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- GERMANY READY TO SUPPORT EU BAN ON RUSSIAN OIL IF IT'S GRADUAL, Bbg

- EC's VON DER LEYEN: WORKING SINCE MARCH TO REDUCE RUSSIA DEPENDENCY .. GAS COMPANIES SHOULD NOT RESORT TO RUBLE PAYMENT .. SAYS RUSSIA MOVE WILL HURT ITSELF, Bbg

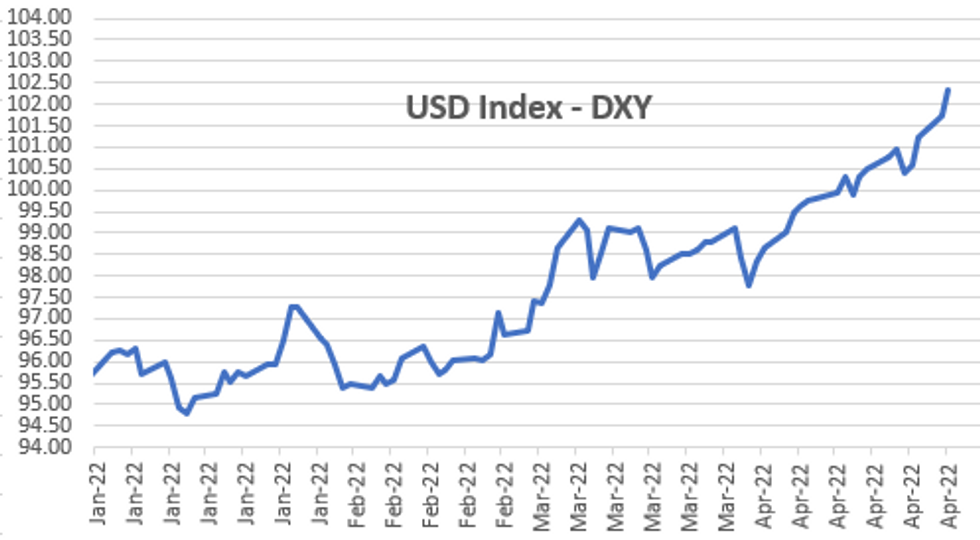

US TSYS: Tsy Turn Weaker Late, US$ Tops Pandemic Peak, Earnings Continue

Rates trade weaker across the board after the bell -- short end support evaporating late as broader markets watch the surge in US$ strength, DXY $ index +.684 at 102.986 vs. 103.282 high -- 5-year highs as it breached pandemic peak of around 102.992 earlier.

- Confluence of likely drivers: ongoing adjustment in Fed tightening cycle - rush to neutral, safe haven, month-end, and knock on efforts from PBoC to counter CNY strength/promote domestic growth all amid lack of market depth.

- FI futures had traded firmer after huge miss in March goods trade balance this morning: record deficit of -125.3B vs -106.3B expected. While exports climbed 7.2%, imports surged 11.5% MoM.

- Curve steepening had already been underway prior to the mildly weak 5Y auction (2.785% high yld vs. 2.777 WI), primary dealer take-up of 16.52% said to "soften the sting" of drop in bid-to-cover from 2.53x to 2.41x.

- Late focus turned to slew of new earnings after the close: Invitation Homes (INVH), Raymond James (RJF), Qualcomm (QCOM), Amgen (AMGN), Ford (F), Meta (FB), PayPal (PYPL) to name a few.

- On tap for Thursday: Weekly Claims, GDP, KC Fed Mfg index and $44B 7Y Note Sale.

US

FED: BNP Paribas: How Many 50bp Hikes Will Powell Tee Up? BNP expects the Fed to hike 50bp and officially announce balance sheet runoff at the May meeting. Powell's could guide on moving rates to/above neutral this year.

- Statement: Could telegraph preference to front-load 50bp hikes with hinting at, for example, an "expedited pace" of rate increases.

- Press conference: Powell will likely "communicate an increasing preference for a front-loaded rate hiking cycle. Expect him to reiterate the prioritization of price over activity data to drive policy." BNP sees potential Powell guidance on preconditions warranting a downshift back to a 25bp pace "could signal upside risks" to a core scenario of 50bp hikes in just May and June, "if he ties the downshift to improvements in inflation and labor market data (which we do not expect until later in the year at best), or similarly if he links it to reaching a neutral policy stance."

- Powell "could provide information that could come more explicitly in the meeting minutes that reveals officials' increasing willingness to go above neutral this year".

- Future action: 225bp of hikes this year, including 50bp in June, but risks tilt toward more 50bp moves. QT risks are "asymmetric", tilting toward slower pace.

OVERNIGHT DATA

- US advance March goods trade balance -125.3B vs -106.3B expected

- US wholesale inventories for March 2.3% versus 1.5% estimate

- US NAR MAR PENDING HOME SALES INDEX 103.7 V 105 IN FEB

- US NAR MAR PENDING HOME SALES -1.2% MOM; -8.2% YOY

- US NAR MAR PENDING HOME SALES INDEX 103.7 V 105 IN FEB

- US EIA:CUSHING STOCKS +1.3M TO 27.4M BARRELS IN APR 22 WK

- US EIA:CRUDE OIL STOCKS EX SPR +0.69M TO 414.4M APR 22 WK

- US EIA:DISTILLATE STOCKS -1.45M TO 107.3M IN APR 22 WK

- US EIA:GASOLINE STOCKS -1.57M TO 230.8M IN APR 22 WK

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 149.76 points (0.45%) at 33390.27

- S&P E-Mini Future up 15.75 points (0.38%) at 4186.75

- Nasdaq up 22.6 points (0.2%) at 12512.5

- US 10-Yr yield is up 9.8 bps at 2.8183%

- US Jun 10Y are down 8.5/32 at 119-25

- EURUSD down 0.0079 (-0.74%) at 1.0559

- USDJPY up 1.06 (0.83%) at 128.29

- WTI Crude Oil (front-month) up $0.03 (0.03%) at $101.74

- Gold is down $19.32 (-1.01%) at $1886.13

- EuroStoxx 50 up 13.28 points (0.36%) at 3734.64

- FTSE 100 up 39.42 points (0.53%) at 7425.61

- German DAX up 37.54 points (0.27%) at 13793.94

- French CAC 40 up 30.69 points (0.48%) at 6445.26

US TSY FUTURES CLOSE

- 3M10Y +12.842, 198.268 (L: 184.219 / H: 198.777)

- 2Y10Y -1.368, 22.536 (L: 16.995 / H: 25.491)

- 2Y30Y -3.237, 31.27 (L: 25.889 / H: 36.931)

- 5Y30Y -0.702, 8.432 (L: 4.768 / H: 13.342)

- Current futures levels:

- Jun 2Y down 0.875/32 at 105-19.125 (L: 105-18 / H: 105-24.5)

- Jun 5Y down 3.25/32 at 113-3.75 (L: 113-03.5 / H: 113-19)

- Jun 10Y down 9/32 at 119-24.5 (L: 119-24 / H: 120-18.5)

- Jun 30Y down 27/32 at 141-19 (L: 141-16 / H: 143-09)

- Jun Ultra 30Y down 1-09/32 at 161-26 (L: 161-19 / H: 164-15)

US 10Y FUTURES TECH: (M2) Corrective Cycle

- RES 4: 123-04 High Mar 31 and a key resistance

- RES 3: 122-12+ High Apr 4

- RES 2: 121-09 High Apr 14 and key resistance

- RES 1: 120-19+ 20-day EMA

- PRICE: 120-00 @ 1200ET Apr 27

- SUP 1: 118-08 Low Apr 22 and the bear trigger

- SUP 2: 118-02+ 0.618 proj of the Mar 7 - 28 - 31 price swing

- SUP 3: 117-22+ Low Nov 8 2018 (cont)

- SUP 4: 116-28 0.764 proj of the Mar 7 - 28 - 31 price swing

Recent gains in Treasuries are considered corrective and the primary downtrend remains intact. Moving average studies continue to point south and fresh cycle lows last week confirmed a resumption of the primary downtrend and an extension of the price sequence of lower lows and lower highs. Scope is seen for a move towards 118-02+ next, a Fibonacci projection. The 20-day EMA is the resistance to watch, at 120-19+.

US EURODOLLAR FUTURES CLOSE

- Jun 22 +0.010 at 98.150

- Sep 22 -0.010 at 97.355

- Dec 22 -0.035 at 96.915

- Mar 23 -0.040 at 96.705

- Red Pack (Jun 23-Mar 24) -0.055 to -0.045

- Green Pack (Jun 24-Mar 25) -0.04 to -0.03

- Blue Pack (Jun 25-Mar 26) -0.04 to -0.035

- Gold Pack (Jun 26-Mar 27) -0.05 to -0.045

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00528 to 0.32486% (-0.00157/wk)

- 1M +0.01500 to 0.76371% (+0.06028/wk)

- 3M +0.00072 to 1.23886% (+0.02515/wk) ** Record Low 0.11413% on 9/12/21

- 6M -0.00142 to 1.82629% (+0.00258/wk)

- 12M -0.00215 to 2.54414% (-0.06257/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $73B

- Daily Overnight Bank Funding Rate: 0.32% volume: $261B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.27%, $897B

- Broad General Collateral Rate (BGCR): 0.30%, $338B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $326B

- (rate, volume levels reflect prior session)

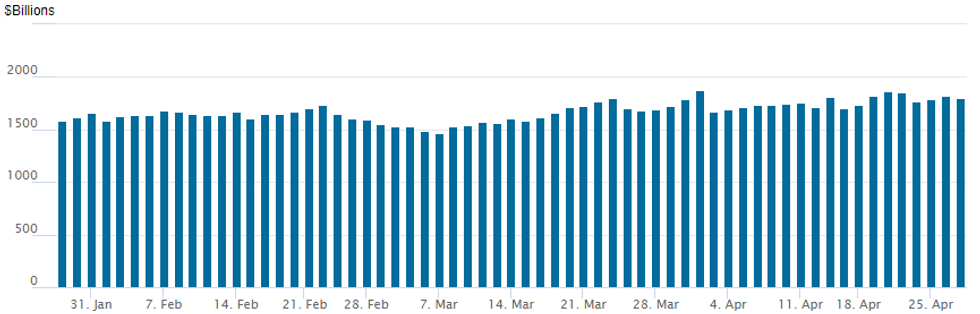

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to 1,803.162B w/ 82 counterparties from prior session 1,819.343B. Compares to all-time high of $1,904.582B on Friday, December 31.

PIPELINE

Expect surge in issuance as stocks work through current earnings cycle.- Date $MM Issuer (Priced *, Launch #)

- 04/27 No new issuance Wednesday;

- Well off last week's pace only $5.3B Priced Tuesday.

- 04/26 $1.3B *Anthem Inc $600M 10Y +135, $700M 30Y +170

- 04/26 $1.2B *Cintas Corp $400M 3Y +75, $800M 10Y +125

- 04/26 $1B *Kommuninvest 3Y SOFR+25

- 04/25 $1B *ST Engineering $700M 5Y +68, $300M 10Y +105

- 04/26 $800M *SVB Fncl $350M 6NC5 +155, $450M 11NC10 +180

- 04/26 $500M Development Bank of Kazakhstan 3Y investor calls

- 04/25 $Benchmark American Express investor calls

EGBs-GILTS CASH CLOSE: Peripheries Underperform

Periphery EGB spreads widened Wednesday as Bunds strengthened on a continued flight to safety. The UK curve was mixed, with the short end stronger but 10+ year segment slightly weaker.

- The bigger moves Wednesday were in the currency market, with EUR and GBP weakening sharply against the USD (in accordance with the risk-off theme).

- Greek spreads widened sharply amid a 5Y GGB tap via syndication, while BTP/Bunds had widest closing level since June 2020.

- German inflation data takes focus Thursday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 4.9bps at 0.1%, 5-Yr is down 4.7bps at 0.529%, 10-Yr is down 1.4bps at 0.801%, and 30-Yr is up 1.9bps at 0.974%.

- UK: The 2-Yr yield is down 1.1bps at 1.489%, 5-Yr is down 0.2bps at 1.575%, 10-Yr is up 1.6bps at 1.812%, and 30-Yr is up 3.3bps at 1.937%.

- Italian BTP spread up 3.2bps at 177.2bps / Greek up 5.6bps at 223.4bps

FOREX: US Dollar Reigns Supreme, USD Index Rises To 5-Year High

- Gas flows across eastern Europe were the early focus of trade following reports late yesterday that Poland and Bulgaria had been cut off from Russian gas supply. The news continued to add headwinds for the Euro, with overall greenback strength exacerbating the EURUSD downward momentum.

- A continuation lower was evident throughout Wednesday following the breach of the 2020 low at 1.0636 and then 1.0577, the lower band of a moving average envelope. The low print of 1.0515 came within close proximity of the next support at 1.0494, Low Feb 22, 2017.

- After trading sharply lower on Tuesday, GBPUSD is also extending the current downtrend. The pair has cleared 1.2676 last printed in September 2020. Today’s low of 1.2503 provided firm support ahead of the psychological level and 1.2495, a Fibonacci retracement.

- In a reversal of yesterday's outperformance, JPY is the poorest performing currency in G10, helping USD/JPY climb back above the Y128.00 level. USDJPY remains in an overarching consolidation phase as bulls pause after the recent rally. This sideways activity highlights the formation of a bull flag, reinforcing bullish conditions with the uptrend still intact.

- Broad greenback strength saw the DXY (+0.55%) break above the 2020 peak to reach the best level since January 2017. However, a firmer day for equity/commodity indices saw the likes of AUD and CAD relatively outperform.

- Focus on the Bank of Japan meeting/decision overnight. Given the BoJ’s continued (and understandable) insistence that current inflationary pressures are cost-push not demand-pull related, markets expect the Bank to leave its monetary policy settings unchanged at the end of its April monetary policy meeting.

- Tomorrow brings flash April CPI estimates from Germany and Spain. The US data calendar will feature Q1 Advance GDP.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/04/2022 | 0130/1130 | ** |  | AU | Trade price indexes |

| 28/04/2022 | 0600/0800 | ** |  | SE | Retail Sales |

| 28/04/2022 | 0600/0800 | *** | | SE | GDP |

| 28/04/2022 | 0700/0900 | ** | | SE | Economic Tendency Indicator |

| 28/04/2022 | 0700/0900 | *** |  | ES | HICP (p) |

| 28/04/2022 | 0700/0900 |  | EU | ECB de Guindos Presents Annual Report 2021 | |

| 28/04/2022 | 0730/0930 | ** | | SE | Riksbank Interest Rate |

| 28/04/2022 | 0800/1000 | *** |  | DE | Bavaria CPI |

| 28/04/2022 | 0800/1000 | | EU | ECB publishes May economic bulletin | |

| 28/04/2022 | 0800/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 28/04/2022 | 0800/1000 | ** | | IT | ISTAT Business Confidence |

| 28/04/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/04/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 28/04/2022 | - |  | JP | Bank of Japan policy meeting | |

| 28/04/2022 | 1230/0830 | * |  | CA | Payroll employment |

| 28/04/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 28/04/2022 | 1230/0830 | *** | | US | GDP (adv) |

| 28/04/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 28/04/2022 | 1400/1600 | | EU | ECB Elderson Panels ECOSOC UN Forum | |

| 28/04/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 28/04/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 28/04/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 28/04/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 28/04/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.