Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GILTS

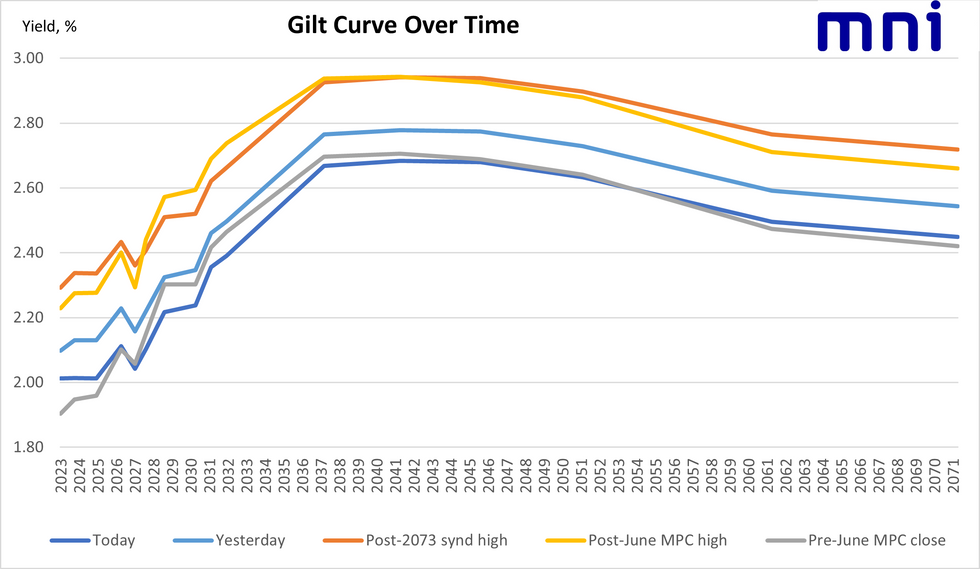

- As noted earlier, gilts have moved higher today. Initially driven by misses in European PMIs, but then finding a little stability as the UK PMI didn't come in quite as weak as the European data had suggested. The UK PMI also pointed to a strong labour market and continued inflationary pressures, meaning the reasons for hikes remain in place (albeit as we have long argued, not at the pace markets had priced - we still see around a 60% probability of a 50bp hike in August with the alternative a 25bp hike - markets still after today's data price 53bp for August).

- Yields at the very front-end of the gilt curve remain higher than the post-June MPC reaction, as do 30+ year yields, but between 5-30 years, yields are now lower than the initial reaction.

- As well as PMI data, this morning saw the release of public sector finance data which weren't market moving but saw borrowing at higher levels than expected.

- Overnight tonight we will receive consumer confidence data for June ahead of tomorrow morning's retail sales print for May. These will give a further update on the state of the consumer following the increase in NICs and the energy price cap - both of which came into effect in April.

- Tomorrow afternoon will see another speech from BOE Chief Economist Huw Pill on ‘Inflation and Debt – Challenges for Monetary Policy after Covid-19’ - an interesting topic but he has already made several appearances since last week's MPC meeting so it is unclear whether he will give much new immediate policy-relevant guidance. MPC member Jonathan Haskel also appears on a panel on the global economy tomorrow.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok