Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUD

AUD/USD saw modest outperformance post the Asia close. We initially tracked to fresh lows just ahead of 0.6710, before rebounding. We got close to 0.6780, before settling back sub 0.6760 into the NY close, which is where we currently sit.

- The DXY is slightly lower, as EUR/USD has edged slightly away from the parity level with the USD. This likely aided the AUD at the margin.

- Cross asset signals were generally negative for the AUD though, with US equities weaker, while the VIX index rebounded further to +27.

- Commodities remained on the back foot, with a lot of the focus on the fresh slump in oil (Brent back sub $100/bbl). The A$ has outperformed oil-related FX over the past 24 hours. AUD/CAD is back to 0.8800, versus recent lows of around 0.8750.

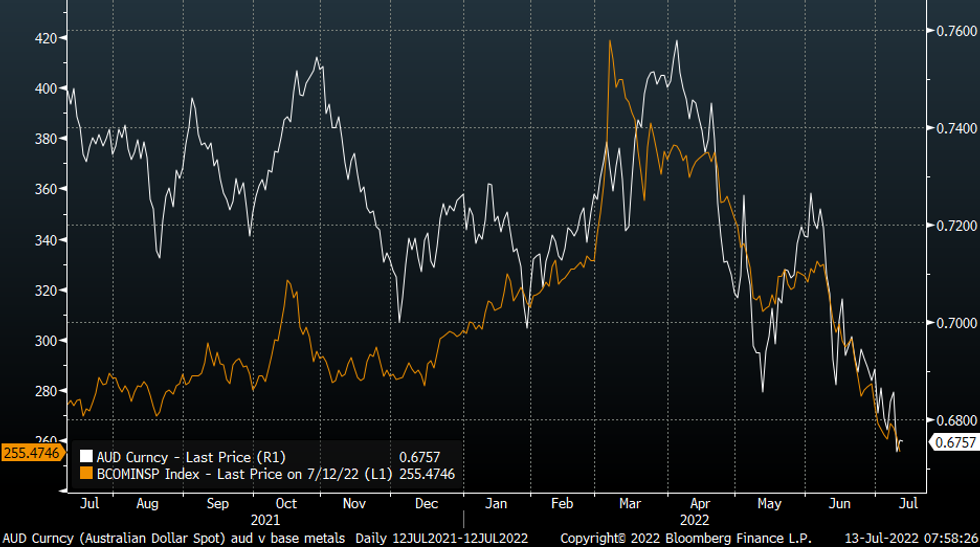

- Base metals also fell further though, down over 2% in terms of the aggregate Bloomberg index. Copper lost over 4% to be sub $330 (CMX basis). The A$ has followed base metal trends fairly closely in recent months, see the chart below.

- Iron ore dipped to $104/tonne, fresh YTD lows, before sentiment stabilized. Steel futures in China were down just over 2.8% yesterday.

- US yields tracked lower, although not as much as seen in the EU, following the weaker German ZEW print. AU-US2yr spreads were range bound yesterday between -50bps to -55bps.

- There is no Australian data out today, but watch for spill over from the RBNZ decision in NZ. A 50bps hike is widely expected.

Fig 1: AUD/USD & Base Metals

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok