Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUD

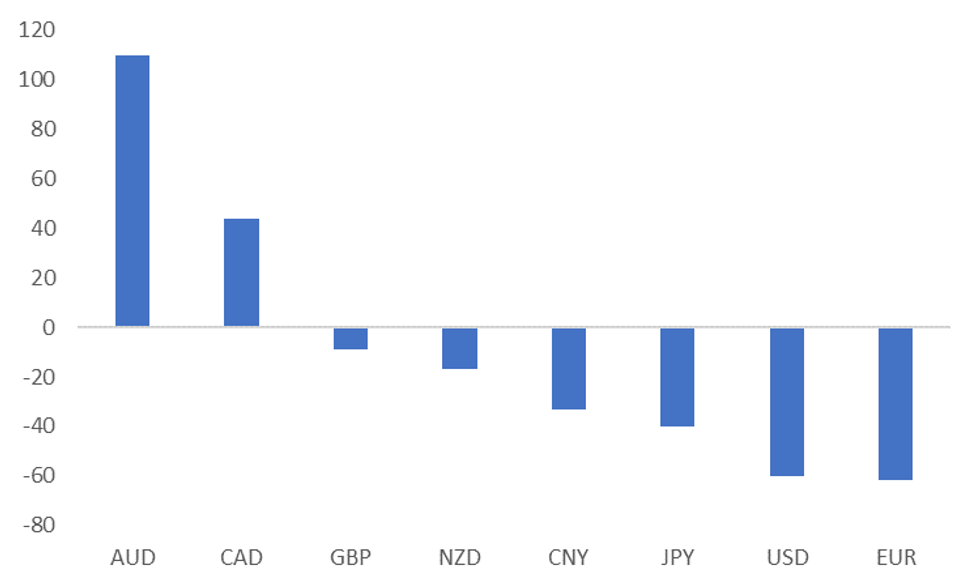

Relative data momentum remains in the AUD's favor. Amongst the major economies and other commodity currencies, Australia's Citi EASI reading is comfortably the highest, see the first chart below. This is likely helping A$ outperformance, which is second only to CAD within the G10 FX space over the past month in terms of spot returns. However, we remain mindful that global recession concerns can still influence the currency, particularly via the commodity price channel.

- Overnight, the much weaker than expected US Philly Fed survey sent the US Citi EASI tumbling, unwinding a chunk of the recent improvement. As the first chart below highlights, all the major economy EASIs are comfortably in negative territory.

- The resilience of the Australian EASI likely reflects less tightness in financial conditions (particularly compared to the US) and less idiosyncratic shocks (like the Ukraine conflict and the EU).

- This relative performance is also being reflected in yield differentials as well. The AU-US 2yr spread is back to -36bps, from recent wides at -60bps. The same holds against the other major economies, (EU, UK and JP), although we are below June highs in terms of the differential.

Fig 1: Major Economy & Commodity Currency Citi EASIs

Source: Citi/MNI - Market News/Bloomberg

Source: Citi/MNI - Market News/Bloomberg

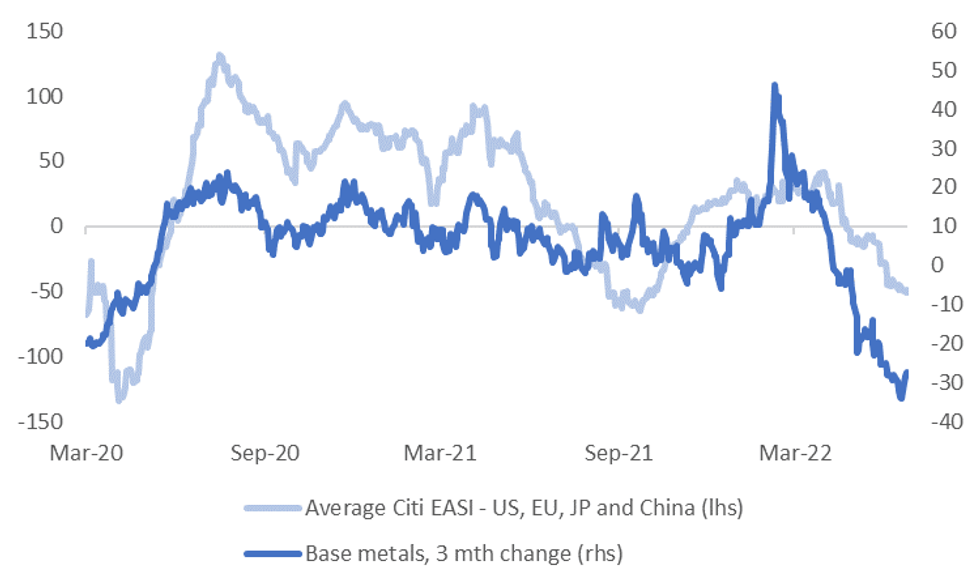

- Recessionary fears can still derail A$ outperformance. The second chart below plots the average EASI reading for the US, EU, JP and China, against the 3 month change in base metal prices. Weaker growth outcomes in the major economies should hurt cyclically sensitive commodities, all else equal.

- There is also a sense that AU data momentum could play some catch up to the downside, as domestic financial conditions tighten. Next week we get June retail sales data. This is likely to be overshadowed by Q2 CPI data though, which could still surprise on the upside given the recent experience in NZ, where Q2 inflation data was stronger than expected.

Fig 2: Major Economy EASIs & Base Metal Prices

Source: Citi/MNI - Market News/Bloomberg

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok