Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUD

AUD/USD remains below the 0.6700 level. The pair was last around 0.6680/80, up from earlier lows in the 0.6660/70 region. Early session highs near 0.6725 remain intact. Note the simple 100-day MA comes in at 0.6701, so this may be offering some short-term resistance. The cumulative 4.2% gain through Thursday/Friday sessions from last week may also be generating some profit taking flows.

- Cross asset signals are mixed. Yield differentials are down slightly, the AU-US 2yr back to -124bps, following hawkish Fed comments earlier. However, we still well above pre-US CPI lows from last week (-140bps).

- In equities we down from best levels from a regional equity market standpoint, although HK/Chia related markets are still up. US equity futures are also lower by around -0.30-50%.

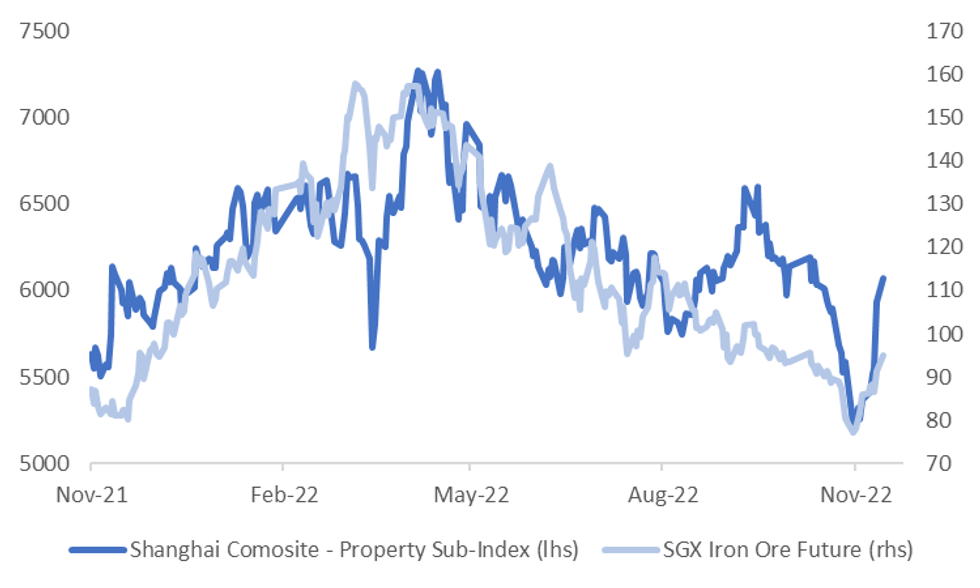

- The Shanghai Composite Property Sub-Index is up around 2.5% at this stage, but this down from earlier highs (close to +5%). The chart below overlays this index against SGX iron ore futures prices. Iron ore prices are around $94/tonne, down from highs of $96/tonne earlier.

- Both series are comfortably off recent lows, but well-down on earlier YTD highs. Further upside, particularly in iron ore, will boost the A$'s valuation appeal. The focus is likely to rest on how much traction China’s recently announced property support measures gain in stabilizing the sector.

Fig 1: Shanghai Composite Property Sub-Index Versus Iron Ore Futures

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok